Last week, we shared extensive empirical evidence that the US housing market is starting to crack when we quoted regional managers from John Burns Real Estate Consulting, all of whom agreed on one (or more) of three things: i) Demand is slowing, namely entry-level due to payment shock; ii) Investors are pulling back; and iii) Ripple effect of rising rates starting to hit move-up market. Here are some excerpts:

Dallas builder: “Interest lists are shrinking or buyers are truly pausing.”

Houston builder: “Many first-time buyers simply no longer qualify with the increase in interest rates, as their debt-to-income ratio gets out of whack.”

San Antonio builder: “Traffic has been cut in half since the hike in rates.”

Raleigh builder: “Investor activity has slowed dramatically.”

Provo builder: “Investors are evaluating the investment more critically than in the past.”

Washington DC builder: “Traffic half what it was in March. Worried about first time buyers. Many fewer REAL buyers than number of people collected on interest list last 6 months. Certainly more attempts [from buyers] to negotiate.”

Seattle builder: “Pause by a large population of buyers. To achieve our desired [sales] pace, we had to make price adjustments. Rates starting to knock people out of qualification.”

Needless to say, a housing crash would be a bad thing for the US economy for which the housing sector is of paramount importance: a house is usually the biggest asset in American’s savings, comprises a large chunk of the labor force, and is a large contributor to inflation indices. That's precisely why the Fed, hell bent on tipping the US economy into a recession as fast as possible to reverse inflation, would want nothing more than a housing recession.

But what if Powell instead gets a housing crash on par with 2007?

If that's what is coming, we may be able to sniff it out soon in this big week for housing data in a US housing market which has been, until now, red hot. As DB's Jim Reid writes, today’s data showed that building remains strong, with houses under construction hitting an all time high, even if pending home sales tumbled as did mortgage applications.

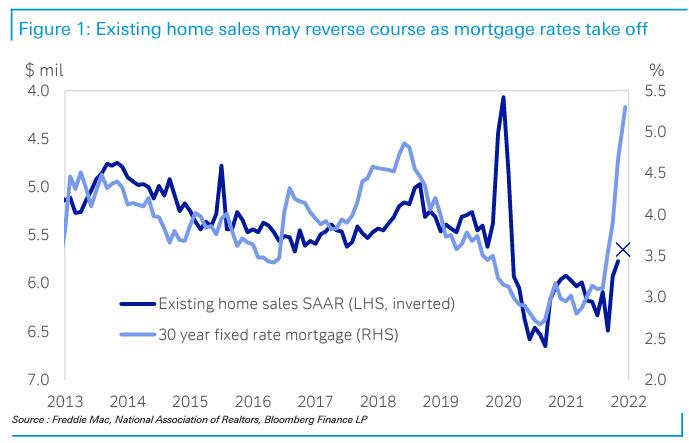

Tomorrow it gets even more interesting: on Thursday morning we get a look at how new home construction translates to sales, which, given the precipitous climb in mortgage rates, could start facing some demand destruction. Which brings us to today's Chart of the Day from Reid, which shows that mortgage rates have taken off with the Fed’s pivot, and the post-Covid boom in existing home sales has started to wobble. Meanwhile, consensus expectations marked by the X show they will decline further tomorrow.

If the chart is correct, Reid warns that "it will be a very painful few months ahead" (for homeowners, not so much for investors as the stock market will sniff out the coming recession and soar, as it frontruns the Fed's next easing).

Of course, the bulls will still point to the strong fundamentals which underly housing: like other sectors, there is a big supply versus demand imbalance as inventories available for sale are still near historic lows, labor in the construction sector is constrained with immigration down, and millennials are aging into their peak earning and home-buying years. All while consumer balance sheets are strong.

So, as Reid concludes rhetorically, will the Fed need to lift rates such that mortgages are far above levels most home buyers have grown accustomed to, ultimately slowing blistering price growth? Or will the cracks appear much sooner (spoiler alert: yes).

One thing is certain: Housing, and its fate, will serve as the earliest guide to the Fed, rates and the US economy.

No comments:

Post a Comment