The post-lockdown spending frenzy may contribute to a sharp rise in inflation, but Ed Yardeni believes the economy can handle it.

Yardeni, who spent decades on Wall Street running investment strategy for major firms including Prudential and Deutsche Bank, sees inflationary pressures as a temporary byproduct tied to massive reopenings and historic liquidity.

“People are just going to keep spending,” the Yardeni Research president told CNBC’s “Trading Nation” on Friday. “A lot of pent-up demand is getting satisfied here both in goods and services.”

Wall Street got further confirmation last week of strong inflation growth through the core personal consumption expenditures, a key gauge closely followed by the Federal Reserve. It rose a faster-than-expected 3.1% in April from a year earlier.

“When the lockdown restrictions were gradually lifted, we did see this tremendous surge in shopping, and shopping does release dopamine in the brain,” said Yardeni. “A lot of people just ran out and started doing shopping.”

First it was goods, and now it’s services, according to Yardeni.

“A lot of services were really eliminated in terms of what was open,” he noted. “Clearly, we’re seeing the services opening up.”

Yardeni expects upward pressure on inflation to last at least a few months.

“The economy has a V-shaped recovery, and actually we’re back to where real GDP was right before the pandemic,” he said. “I would expect to see some slowing down in the economy later this year going into next year.”

He anticipates demand will eventually wear off even in the housing market where prices are booming.

“I can’t imagine that the kind of growth rates that we’ve been seeing over the past few quarters are sustainable,” said Yardeni.

But when it comes to rents, Yardeni sees landlords getting more pricing power. He finds the rental market is tightening up pretty quickly right now.

“We’ve kind of run out of an inventory of houses. All these people were hoping to buy something affordable and finding that prices are up 20% from a year ago, and there’s slim pickings,” he added. I’m concerned a lot of would-be homebuyers are just saying ‘You know what, no mas. I give up. Let’s just stay.’”

What’s next for Treasury yields

Yardeni, a long-time stock market bull, believes the benchmark 10-year Treasury Note yield will remain rather benign despite surging prices.

“It’s been remarkably stable in the past few months... in the face of higher than expected inflation news and lots of very strong economic indicators,” he said. “I do think we’re going to see 2% on the bond yield.”

It’s not a level that should spook Wall Street, according to Yardeni. However, he predicts Federal Reserve policymakers will start talking about tapering earlier than investors think. As a result, he sees the 10-year yield ending 2022 around 2.5% to 3%.

“Not exactly the end of the world because that’s where bond yields were before the pandemic,” Yardeni said. “That would actually be going back to normal.”

The 10-year yield ended the week at 1.58%, down almost 6% over the past two months.

Economists and policy makers are debating whether stimulus spending and easy monetary policy are fueling inflation. Many businesses say there is another culprit that should share the blame: import tariffs.

The Trump administration implemented tariffs on products including lumber, steel and semiconductors to shield American companies from a glut of cheap imported products from China and other countries.

The tariffs have long been opposed by U.S. companies that import the goods and pay the levies. They are making a new push for the Biden administration to lift them, on grounds that tariffs contribute to rising prices and product shortages that are accompanying the post-pandemic recovery.

“I have had 15 price increases from my primary steel supplier since September,” said Scott Buehrer, president of B. Walter & Co., a Wabash, Ind., maker of fabricated metal products. “What’s the justification for these tariffs when you have sky-high steel prices?”

Some economists say the tariffs have had only muted effects on prices and that their removal won’t do much to ease the price pressure.

Mr. Buehrer’s company was among more than 300 manufacturers that wrote to Mr. Biden on May 6 asking him to immediately terminate 25% tariffs on steel and 10% levies on aluminum. The Biden administration has said it is reviewing the tariff policy but has no immediate plans to lift the tariffs.

The manufacturers say the tariffs make their companies less competitive at a time when U.S. buyers, facing red-hot domestic demand, are paying 40% more for some steel products than their European peers.

Mr. Buehrer said he has cut his payroll by 10% to reduce costs as the prices of rolled steel nearly tripled since last fall. But labor unions and the steel industry are urging Mr. Biden to keep the metal tariffs in place, saying in a May 19 letter that the policy has enabled the industry to “restart idle mills, rehire laid-off workers and invest in the future.”

“The tariffs have been in place since 2018 and there has been no inflationary pressure since then,“ said Roy Houseman, legislative director at United Steelworkers. “The U.S. has put trillions of dollars of stimulus in the economy. That is going to impart some inflationary pressure.”

Another industry wrestling with soaring prices is home-building.

Futures contracts of lumber in May reached more than $1,600 per thousand board feet—a record that is more than four times the typical price this time of year. The National Association of Home Builders estimates the higher lumber prices have added $36,000 to the price of a typical single-family home.

“It doesn’t make any economic sense to be taxing things when you don’t have sufficient domestic supply,” said Robert Dietz, NAHB’s chief economist. “Appliances, washing machines, literally the nuts and bolts that go into making a home—screws and nails—are subject to some of the metal tariffs.”

Home builders and lawmakers have pressed Mr. Biden to eliminate tariffs imposed in 2017 on Canadian softwood lumber, part of a decadeslong disagreement between U.S. and Canadian lumber producers.

Instead of removing the duty, the Commerce Department issued a preliminary decision May 21 to double the levy to 18%, concluding that Canadian imports are heavily subsidized. The tariffs will remain at the current 9% until a final decision on the proposed increase is made before November, a Commerce Department official said.

To provide relief from Trump-era tariffs on a broader range of Chinese imports, a bipartisan group of 40 U.S. senators in April asked the Biden administration to restart a process to grant importers exclusions for more than 2,000 items ranging from pillows to auto parts. The exclusion process, introduced by the Trump administration, expired in December but hasn’t been renewed.

When the Trump administration’s tariffs first went into effect, some economists warned they could spur inflation. But there appears to be a consensus that the impact has been muted.

“Given that the tariffs didn’t have a big impact on consumer prices in the first place, I probably wouldn’t expect their removal to result in significant downward pressure either,” said Andrew Hunter, economist for Capital Economics, a research firm.

The muted impact is partly because tariffs only affect imports, which typically make up a relatively small share of the domestic market. For steel, imports represent roughly one-third of the total U.S. demand. And the share of the taxed imports is even smaller as the largest exporters to the U.S.—Canada, Brazil and Mexico—are exempted.

Import prices of the goods subject to tariffs did rise initially. But many importers absorbed much of the increases, rather than pass the full increase on to consumers. Meanwhile, the prices of many goods not subject to the tariffs were declining, keeping the overall inflation rate low.

David Weinstein, a Columbia University economist, says tariffs may actually lower prices over the long term.

Mr. Weinstein and his colleagues examined changes in financial markets’ inflation expectations based on bond-market yields around the time of 11 new tariff announcements by the U.S. and China between 2018 and 2019.

To their surprise, he said, they found that the events lowered inflationary expectations so that prices were expected to be roughly 1 percentage point lower five years later and 1.3 points lower 10 years later. Stock prices also fell.

“What the markets are predicting, and our data is suggesting, is that the trade war will have negative impacts on productivity,” he said, referring to tariffs’ hit to companies’ operations. “When you hold down productivity, you’ll have really big impacts down the road on the success of your economy, and prices as well.”

The U.S. Trade Representative’s Office, which is conducting a review of U.S. tariff policy, is studying whether easing tariffs, among other factors, could relieve the supply shortage for lumber and other products, Cecilia Rouse, chair of the White House Council of Economic Advisers, said during a May 18 briefing.

She added, however, trade policy is a “much bigger issue” than short-term market gyrations and that it needs to be worked out in the context of Washington’s global policy.

Wholesaling real estate is the process of finding a deeply discounted home and passing it along to an end investor. Bearing fast cash, wholesalers are flooding low-income neighborhoods, seeking distressed homeowners who want to sell quickly. Record low mortgage rates,low housing inventory, and a real estate frenzy have increased the amount of wholesaling conducted nationwide since the pandemic as many were lured in by YouTube tutorials.

The entire strategy behind wholesaling is finding a discounted property, get it under contract, and then flip it to an interested buyer for a quick profit. Bloomberg reports some wholesalers are using strong-arm tactics and misinformation to force sales. Wholesaling a house is a strategy unlike flippers, who obtain ownership of the home during the renovation period ahead of the eventual sale. A wholesaler negotiates with homeowners to find an investor (usually a cash offer).

"I don't buy houses. I solve problems," Scott Sekulow, who leads an Atlanta-area congregation of messianic Jews, told Bloomberg. He bills himself as the "Flipping Rabbi." Many of his clients come to him who are distressed. Sekulow can find them an investor who will take over the property to flip for resale.

Sekulow said hedge funds are getting into the game. He told a conference of wholesalers: "When you can get in with them, they're there paying stupid money."

Wholesaling is entirely legal, but advocates for low-income areas say these folks are tricking sellers into deeply discounting their homes.

After residents in Illinois, Oklahoma, Arkansas, Kansas, and the city of Philadelphia, have been bombarded with wholesalers overrunning street corners with "We Buy Houses" signs, local governments have begun to crack down on these types of transactions.

"In my neighborhood in West Philly, I probably get three postcards a month from one of these guys," said Michael Froehlich, an attorney with Community Legal Services of Philadelphia. "If you can get leads, you can dupe somebody into signing a contract for far less than fair market value, and you can make $30,000, $40,000, $50,000 on the house."

Not too long, dozens of wholesalers, flippers, and investors gathered at a DoubleTree hotel in Roswell, Georgia, to meet for the Atlanta Real Estate Investors Alliance conference.

Mike Cherwenka, who was a panelist at the event, refers to himself as the "Godfather of Wholesaling," told the audience:

"Cash is king, and when you can just offer people cash and close within a week, you've got leverage, right?" said Cherwenka. "People perk up and listen when you make an offer and you've got proof of funds right there."

Brian Dally, whose Atlanta-based finance company, Groundfloor, estimates the firm will fund about $350 million in real-estate investments this year. Of that, 40% involve wholesalers.

However, complaints are beginning to mount against aggressive wholesalers who have flooded the industry since last year. Many of these folks are entry-level and don't need real estate licenses which means regulators have very little power over them. Wholesalers say they don't need a license because they're arranging a sale or buying the home in a private transaction to flip to investors.

Froehlich alleges that some wholesalers trick low-income homeowners into believing their home needs tens of thousands in repairs to get a massive discount.

Meanwhile, Philadelphia cracked down on wholesalers last fall by issuing them licenses if they wanted to continue doing business in the metro area. Oklahoma this spring issued licenses for wholesalers. Arkansas and Illinois passed laws in the last couple of years that increases local government's control over wholesaling. More recently, a bill in Kansas to regulate the industry died.

Wholesalers acknowledge they have some bad apples, but most want to revitalize low-income neighborhoods that have been neglected. Sure... it's all about the quick money.

Costs are a major challenge in the affordable housing market segment. The requirement to keep costs down requires multiple funding sources, which lead to fragmented and complex deals that are often too challenging to develop. A new report sponsored by Capital One from the Terner Center for Housing Innovation at the University of California Berkeley highlights the fragmented nature of affordable housing and calls for more streamlined alternatives.

Part of the reason for greater funding complexity is that it has gotten more expensive to build housing, and LIHTC affordable financing is not immune to this, Desiree Francis, head of community finance at Capital One, tells GlobeSt.com. “The number of stacked financing sources needed has risen in tandem with the rapid increase in building costs. These increases are not unique to affordable housing production: the Terner Center’s research found that hard construction costs have driven up costs for both affordable and market-rate developments.”

However, layering financing sources to pursue a deal actually drives up costs, making affordable projects even more out of reach. “In addition to mismatched allocation cycles, individual requirements for funding sources varies, which lengthens the development timeline and contributes to costs increases,” says Francis. “Many developers that the researchers spoke to for the report pointed to the lack of alignment of deadlines among key funding sources as a key contributor to longer timelines and associated cost increases.”

Unfortunately, the problem is getting progressively worse. “The average number of financing sources layered in a LIHTC development has ticked upward in recent years, but the patchwork of funding sources needed tends to vary by credit type, project location, and target population,” says Francis.

Solving the financing problem will require coordination from multiple players, but Francis says that the sector is ready for innovation. “We encourage developers, investors, government and other industry stakeholders to identify and design solutions that create more affordable housing,” she says. “Advocate at the local, state and federal level for policies, processes and practices that drive efficiency, reduce costs and remove barriers in support of addressing the affordable housing crisis.”

Often, affordable financing becomes more complex when it serves the lowest income residents, usually when the budget is already tight. Francis adds, “The lower the target income of the population served by the affordable community, the gap financing needs increases and the more complex the financing tends to become.”

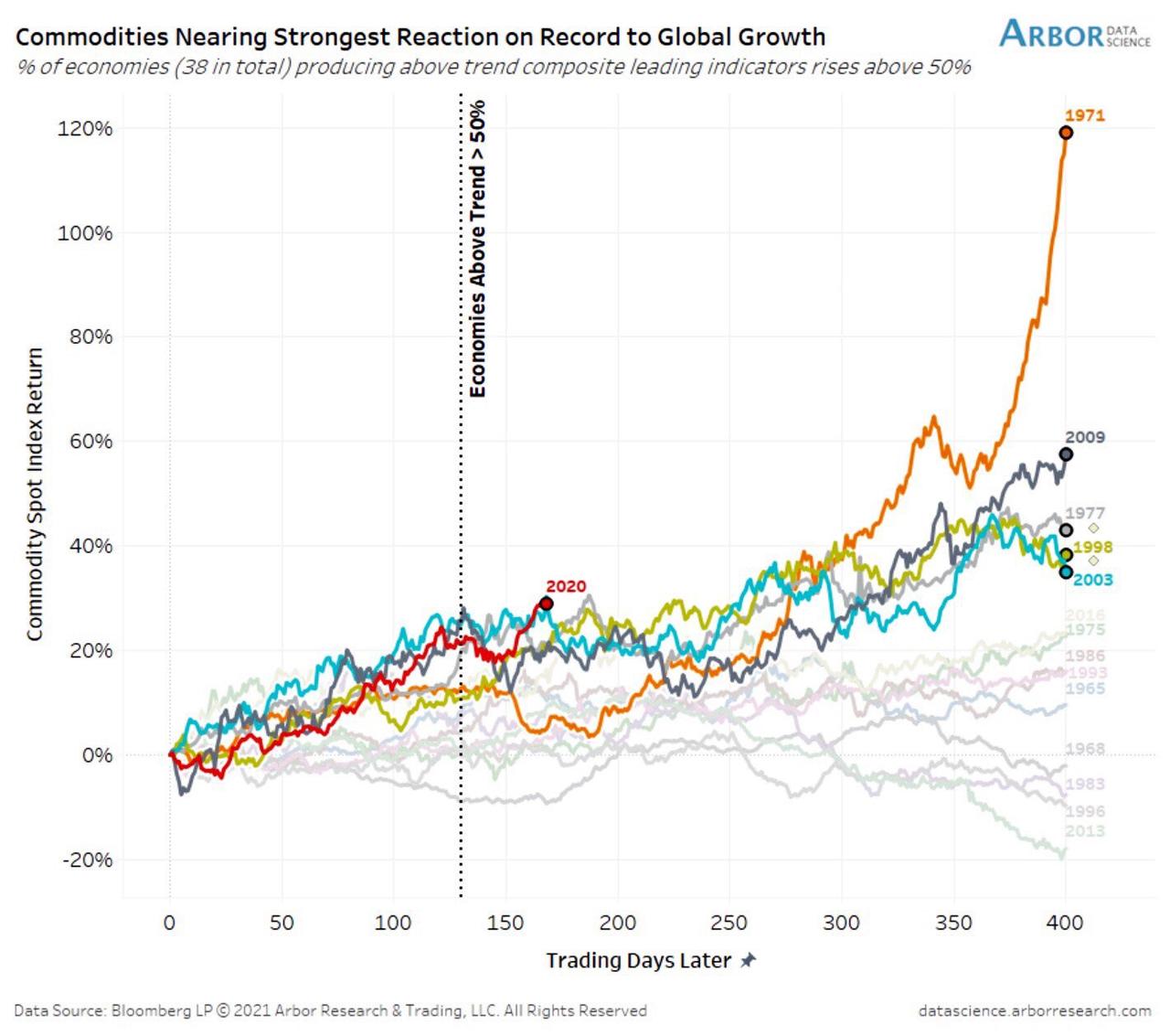

With BofA predicting that the US is facing a period of "transitory hyperinflation" as a result of soaring commodity prices in everything from metals to food...

.... and beyond, in what increasingly more warn is a stagflationary burst right out of the 1970s playbook...

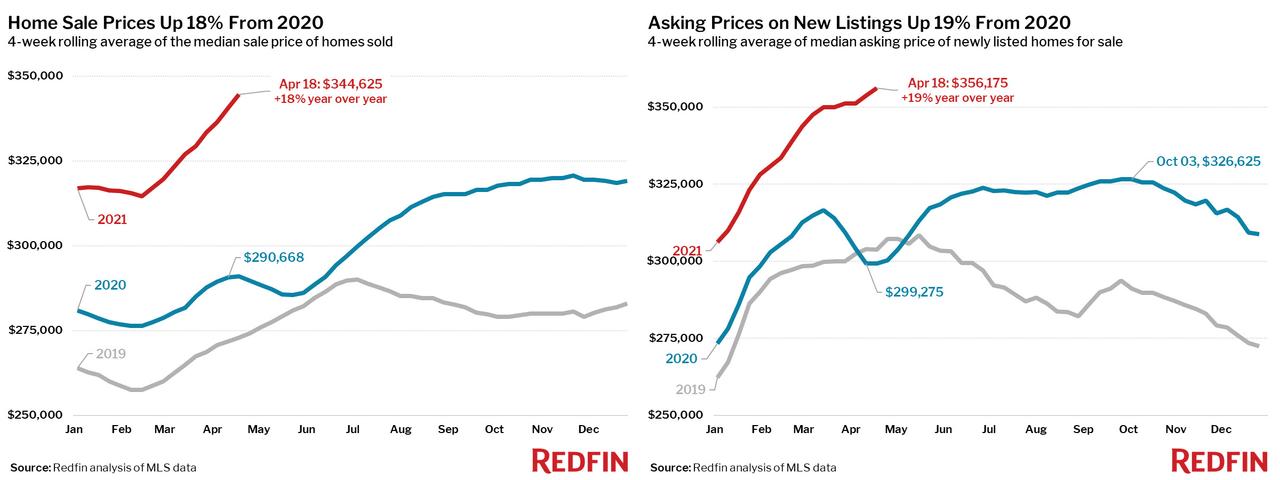

... it makes sense that home prices are also surging thanks to trillions in stimmy checks, near-record low mortgage rates and an exodus away from cities, and as we noted two weeks ago that's precisely what they are doing, with Redfin reporting an 18% jump in median home sale prices to an all time high...

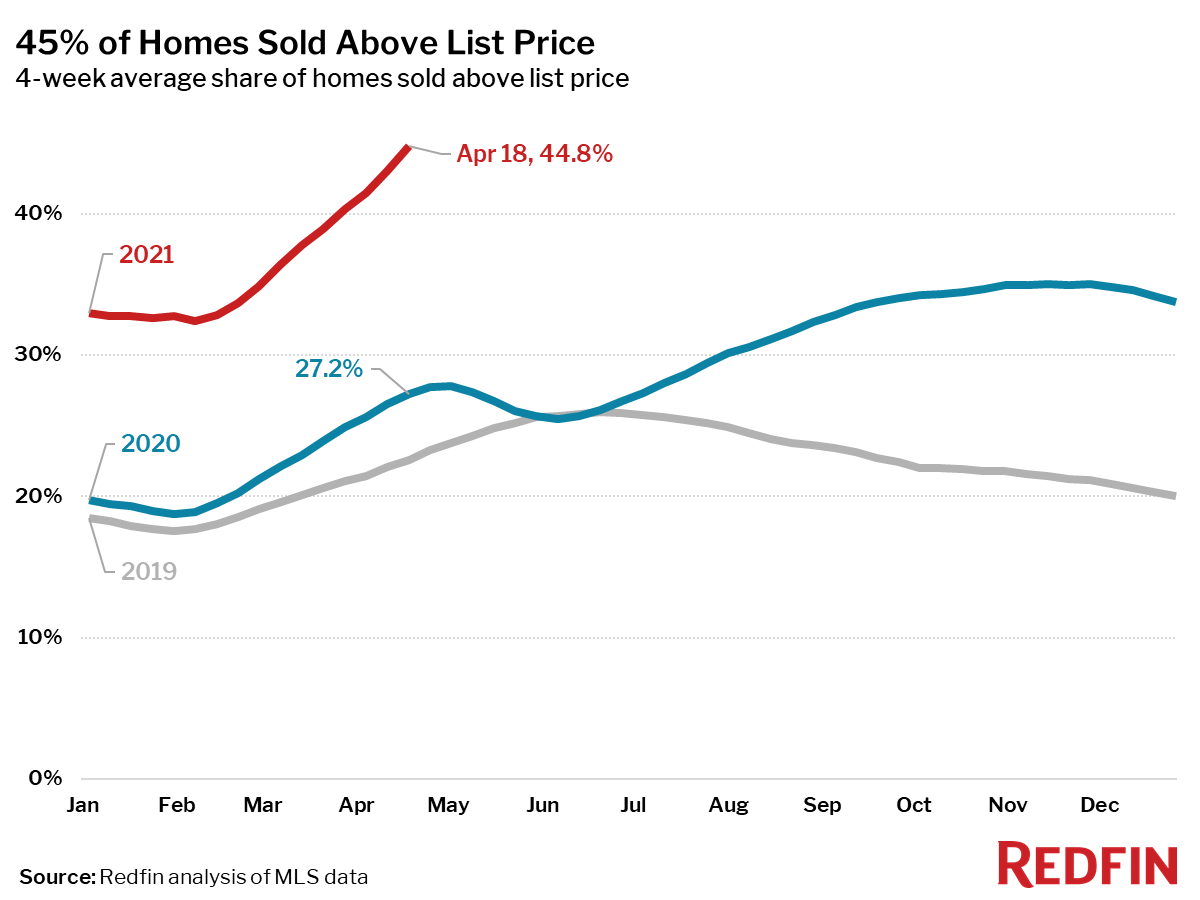

... as a record 58% of all houses sell within two weeks of listing, of which 45% sell for more than their listing price, also a record.

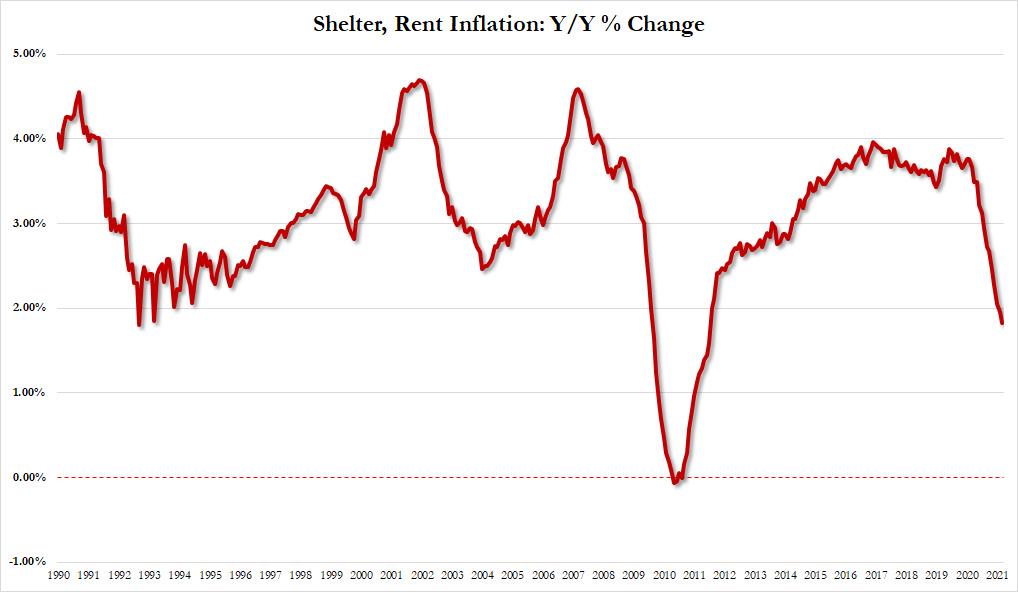

Amid this dismal "transitorily hyperinflationary" landscape, where those whose incomes aren't similarly hyperinflating find themselves at risk of being unable to afford a roof above their head, there was one ray of hope: renting, with rent prices tumbling in recent months and according to the BLS' monthly CPI metric, rent inflation had just dropped to the lowest in a decade, just below 2.0% annually...

... which due to the way the CPI basket is weighted acted as a key anchor on overall CPI rates, and served to distort the broader inflationary picture. In short, the Fed would look at the relatively tame core CPI which was only tame thanks to "tumbling" rents and would conclude that there is nothing to worry about.

Only, as we first discussed three weeks ago, it now appears that not only was the government misrepresenting the actual data in hopes of extracting as much stimulus from the Biden regime by pretending inflation is low and "contained", but that rents are in fact soaring once again.

As we reported at the start of May, American Homes 4 Rent, which owns 54,000 houses, increased rents 11% on vacant properties in April, the company reported in a statement:

... Continued to experience record demand with a Same-Home portfolio Average Occupied Days Percentage of 97.3% in the first quarter of 2021, while achieving 10.0% rental rate growth on new leases, which accelerated further in April to an Average Occupied Days Percentage in the high 97% range while achieving over 11% rental rate growth on new leases.

Invitation Homes, the largest landlord in the industry, also boosted rents by similar amount, an executive said on a recent conference call. Or, as Bloomberg puts it, record occupancy rates are emboldening single-family landlords to hike rents aggressively, testing the limits of booming demand for suburban rentals.

While soaring housing costs had put homeownership out of reach for most Americans, rents had been relatively tame for much of 2020. But in recent months, rents have also soared as vaccines fuel optimism about a rebound from the pandemic, and a reversal in the city-to-suburbs exodus. The increases, as Bloomberg so eloquently puts it, "may add to concerns about inflation pressures."

“Companies are trying to figure out how hard they can push before they start losing people,” said Jeffrey Langbaum, an analyst at Bloomberg Intelligence. “And they seem to be of the opinion they can push as far as they want.”

Fast forward to today when we have definitive proof that the companies were right.

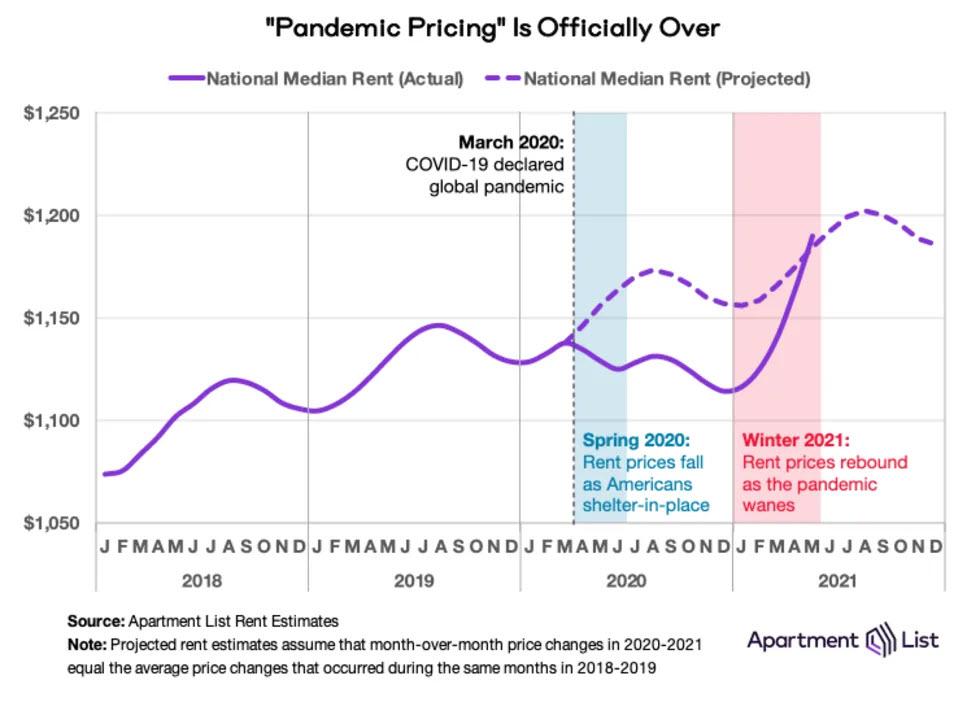

According to the June Apartment List National Rent Report, the national rent index increased by 2.3% from April to May,the largest single month increase ever recorded in AL estimates, which begin in January 2017. It was also the third straight month in which that record has been broken, following a 2.0 percent increase last month and a 1.4 percent increase in March.

In March, prices rebounded to their pre-pandemic levels. This month, we hit a new milestone -- our national index is now above the level where we project it would have been if the pandemic-related price declines of 2020 had never occurred at all.

After this recent spike, year-over-year rent growth now stands at 5.4% nationally, and prices are now above the level where rents would have been if the pandemic-related price declines of 2020 had never occurred at all.

In the chart above, AL plots the national median rent from 2018 to present. The data for 2018 and 2019 depicts the smooth seasonality of a typical year, in which prices peak during the summer busy season and then dip slightly in the winter off-season. Overall, prices increased by 2.9 percent in 2018 and 2.1 percent in 2019. 2020 represents a clear break from this trend, with rents declining in the early months of the pandemic during what is normally peak-season. The dashed line in the chart represents a projection of how rents would have changed over the past year in the absence of the pandemic. This projection is based on an average of the growth rates that we observed in 2018 and 2019. Actual rent growth had been trailing this projection since the start of the pandemic, but this month’s record setting growth has now put actual rents ahead of the projection. Year-over-year rent growth now stands at 5.4 percent, another record.

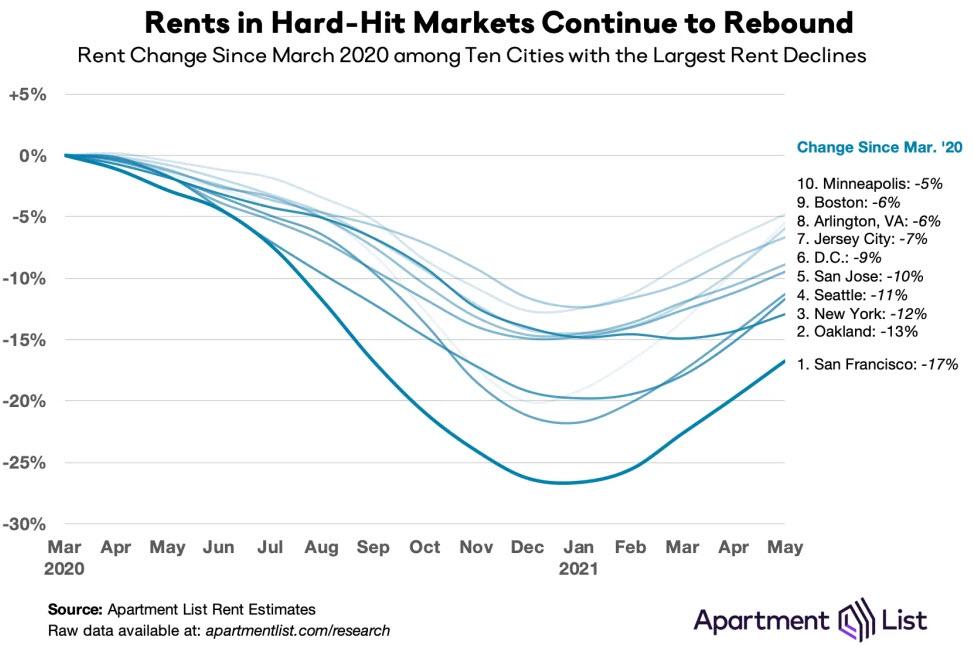

To be sure, there is significant regional variation in rent trends, and prices in a number of markets are still well below pre-pandemic levels. That said, even in these markets, prices are rebounding rapidly. San Francisco headlines throughout the pandemic for the staggering 26.6 percent drop in rents from March 2020 through January 2021, but since January, San Francisco rents have increased by 13.4 percent. Although rents in San Francisco are still 16.8 percent below pre-pandemic levels, the market has clearly turned a corner, and the best deals appear to be behind us.

San Francisco aside, there is a similar trend across the rest of the country where rents had been falling fastest. Nine of the ten cities with the sharpest year-over-year rent declines have now experienced positive rent growth for four consecutive months. Four of these cities -- San Jose, Washington, D.C., Boston, and Minneapolis -- have seen rents increasing for five consecutive months. The following chart shows month-over-month rent growth from 2018 to present for six of the cities that have been hit hardest by the pandemic:

As AL notes, in each of the six cities shown, the fastest single-month rent increase has taken place in 2021. Rents are still below pre-COVID levels in each of these cities, but they’re quickly catching up. Nowhere is the trend stronger than in Boston, where prices have increased by an average of 3.4 percent per month in 2021 - if that pace continues, Boston rents will surpass March 2020 levels by mid-summer.

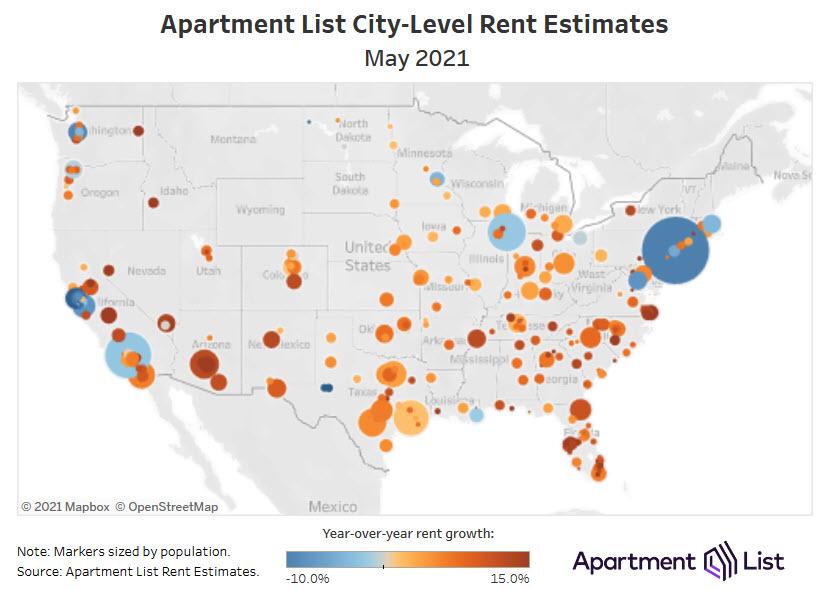

But if prices are rebounding sharply in traditional coastal markets, the market is nothing short of frenzied across another group of mid-sized markets. The pandemic and remote work spurred demand for the space and affordability that these cities offered, and in response, rent prices grew even as the surrounding economy struggled. But while rent declines in expensive markets have reversed course, the cities where rents have been growing fastest are continuing to boom. For the clearest example, no further than Boise, ID where the average rent has soared by 31% in the past year!

As ApartmentList notes, Boise, ID is leading the list, where rents grew by a staggering 6.6% over just the past month. This is the fastest month-over-month growth rate among the nation’s 100 largest cities, and Boise also continues to rank #1 for fastest year-over-year growth, which now stands at 30.8 percent. All of the 10 cities where rents have grown fastest since the start of the pandemic continued to see increases this month.

Many of these markets had been heating up prior to the pandemic. For example, from January 2017 to January 2020, rents in Mesa, AZ increased by 25.5 percent, the fastest growth in the nation over that period. Fresno ranked third for fastest rent growth from 2017 to 2020, while Chandler, AZ ranked sixth. Eight of the ten cities with the biggest pandemic booms were in the top 20 for pre-pandemic growth from 2017 to 2020. The pandemic did not necessarily start a new trend in these markets, so much as accelerate an existing one. This stands in contrast to what has happened in the expensive markets discussed above, for which the rent declines of the past year were a complete aberration. Given this longer-term context, as well as the continued upward trajectory in rent trends, it seems that Boise and cities like it have yet to hit their peaks.

As the Apartment List concludes, the pandemic created some truly "transitory" softness in the rental market last year, and in response, 2021 has seen some of the fastest rent growth we have on record in our data. Nationally, rents have now surpassed the level where they would have been if rent growth had not been disrupted by the pandemic. In markets like San Francisco where rents had been falling fastest, prices have turned a corner and are now rebounding. At the same time, booming markets like Boise continue to see prices climb. More broadly, rental inventory across the nation remains tight, and as vaccine distribution continues to gain momentum, we may be seeing even higher prices as a result of released pent up demand from renters who had been delaying moves due to the pandemic. Whereas last year’s peak moving season was halted by the pandemic, this year’s seasonal spike appears to be making up for lost time.

Summary: surging rents - the "missing piece" from both the CPI and PCE baskets - are back with a vengeance, and the result is that no matter which official inflation metric one uses, we are about to see some truly epic numbers in the coming weeks.

Before the COVID-19 pandemic, Idaho, like many states across the country, faced rising housing costs, low home-vacancy rates and increasing efforts by landlords to evict tenants.

Thanks to increased unemployment benefits, federal stimulus checks and eviction moratoriums—all part of the government's pandemic response—renters' lives improved slightly in 2020. But with those programs decreasing or disappearing, many Idahoans and other Americans who rent their homes will still struggle to pay rent and face imminent risk of being evicted.

Our analysis of eviction rates across the state of Idaho finds that numbers were down in 2020 but are poised to return to—or even exceed—pre-pandemic levels in the coming months as economic support for renting families runs out.

Similar trends in other states could spark a rise in evictions across the nation.

Idaho evictions

In 2016, 2,037 or 1.1% of all renting households in Idaho faced an eviction filing—when a landlord formally requests an eviction order from a court. The courts ordered evictions for 1,107 households, or 0.6% of the state's renting households that year.

Eviction filings that do not end in an ordered eviction may be a result of renters reaching a settlement with the landlord before eviction. Even when dismissed or settled, filings affect a tenant's record, potentially making it challenging to find new housing for years into the future.

By 2019, eviction filings increased to affect 2,673 households, 1.4% of the state's renting households, with 1,611, or 0.8%, ultimately facing a court-ordered eviction. Between 2016 and 2019, housing prices in Idaho increased by 34.7%, while the median income increased by only 17.7%. When housing costs outpace income, affordable housing stock decreases with a likely increase in evictions.

In 2020, however, eviction numbers dropped—1% of Idaho's renting households, 1,893 families, had an eviction filing and 1,127, or 0.6%, were formally evicted.

Unlike other states, Idaho did not have a statewide eviction ban, but there are potential reasons for these decreases.

From March 25 through April 30, 2020, state courts were closed, except for essential hearings—which could have included evictions relating to illegal activity. Most other eviction proceedings would have been delayed. In addition, some landlords may have decided to seek resolutions other than eviction, especially as cash aid came in from federal and state governments.

However, when the courts reopened in May 2020, eviction filings and formal evictions spiked. And monthly statistics show the rates rising almost back to 2019's levels. This raises the question of the ability of federal bans alone to decrease eviction rates.

Federal eviction moratoriums

When the pandemic hit, an estimated 15.9 million people across the country lost their jobs and faced difficulty affording their housing. Public health officials needed people to stay at home to limit the spread of the virus, so governments took action to curb the evictions many feared were imminent.

Federal relief legislation included direct cash payments to most American households, additional unemployment payments, emergency rental assistance and bans on evictions.

The federal Coronavirus Aid, Relief, and Economic Security Act, known as the CARES Act, banned evictions from March 24 through Aug. 24, 2020, but applied to only the relatively small number of renters using federal assistance programs to pay their rent, or living in properties with federally backed financing.

A broader eviction ban, ordered by the Centers for Disease Control and Prevention, took effect on Sept. 4, 2020, and is set to expire on June 30, 2021. It covers more renters, including people who are at risk of moving to overcrowded lodging or becoming homeless. But it's not automatic protection: Tenants must prove their eligibility.

The CDC's eviction ban also faces several court challenges; it was most recently struck down by a federal court in Washington, D.C. – though the decision is on hold pending appeals. So its protection may not last very long.

Making matters more stressful for renters, neither eviction ban forgave unpaid rent, so renters are still responsible for back rent and may face eviction in the future if they cannot pay.

State and local eviction moratoriums

States and cities across the U.S. that set up their own eviction-prevention programs are seeing lower eviction rates than those where tenants were protected only by the federal rules.

Princeton University's Eviction Lab Tracking System gathers eviction data in five states: Connecticut, Delaware, Indiana, Minnesota and Missouri, as well as 28 cities around the country.

Like Idaho, Missouri did not have a statewide eviction ban and saw a similar dip and spike in cases in April and May 2020. Delaware and Indiana had statewide bans and saw sharp increases in eviction filings after the bans expired. Connecticut and Minnesota both have ongoing bans, and eviction rates are far below pre-pandemic levels.

In Idaho, Republican Gov. Brad Little allocated $15 million in federal CARES Act funds to provide rental assistance to households struggling to pay rent because of the pandemic. Another $200 million was added to that fund through the American Rescue Plan Act in 2021. Payments go directly to landlords to offset current and back rent, depending on a household's specific circumstances.

Once these funds run out and the CDC eviction ban expires or is overturned in court, renters throughout the country will have no remaining pandemic-related protections from eviction filings. However, those households may still be feeling the pressure from the pandemic—and may not be able to come up with current rent, much less months of back rent they might also owe.

The aid may be coming to an end, but the potential for an eviction crisis remains—in Idaho, and around the nation.

But none of this has spooked the Fed into conceding - or believing - that inflation is anything more than transitory. And maybe just this once, the Fed has a point because all else equal, by which we mean lack of rising wages, the best cure to higher prices is, well... higher prices.

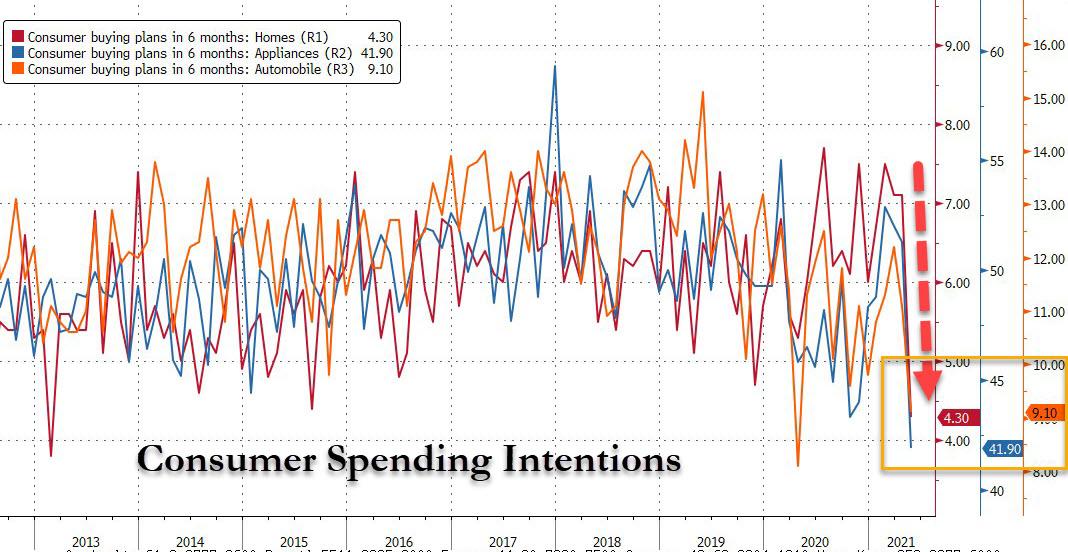

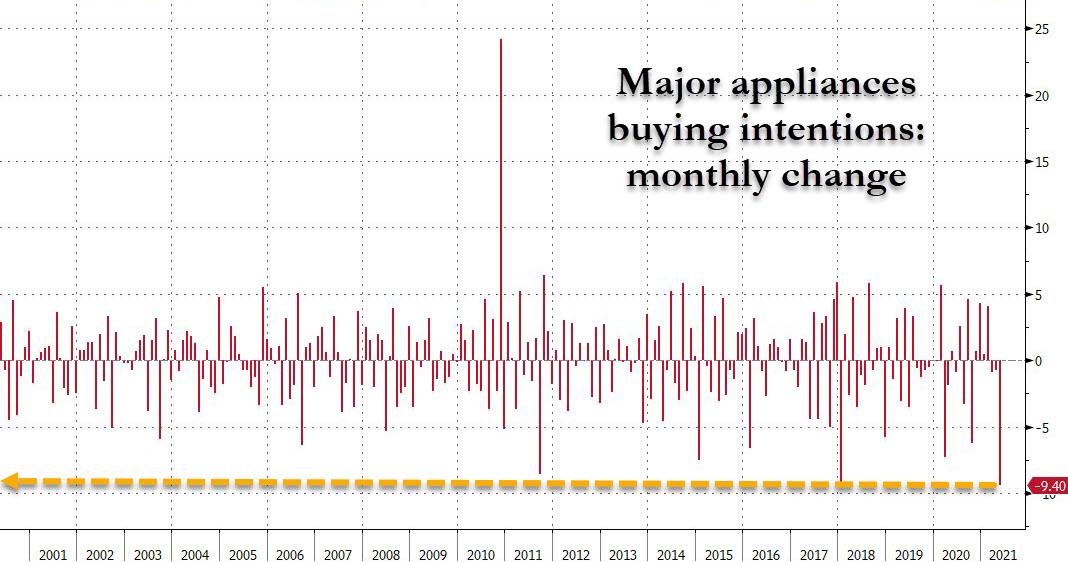

Presenting Exhibit A: understanding that Biden's stimmy bonanza is about to end and that soon they will have to live again within their means, Americans' buying intentions (6 months from today) as measured by the Conference Board, have cratered across the 3 major spending categories: homes, automobiles and major household appliances.

The drop was so massive, it amounted to the biggest one-month drop in intentions to purchase appliances...

... and homes...

This confirms what we noted earlier, namely a record divergence between crashing homebuyer confidence (due to record home prices) and soaring homebuilder confidence (also due to record home prices). Guess which one will matter in the end.

This, for better or worse, screams stagflation: as Lynn Franco, senior director of economic indicators at the Conference Board, said while consumers’ assessment of present-day conditions improved, "consumers’ short-term optimism retreated, prompted by expectations of decelerating growth and softening labor market conditions in the months ahead.”

While it's clear why stagflation will be "worse", we say better because if nothing else these data confirm that US consumers are now tapped out, if not today, then certainly 6 months from today when Biden's trillions in stimmies will have been long spent, and the spending spree will be over.

Oh, and for those saying wage hikes may be permanent we have some bad news: employers know very well that the extended unemployment benefits bonanza ends in September at which point millions of currently unemployed workers will flood back into the labor force sending wages sharply lower, and is why instead of raising base pay, most potential employers offer one-time bonuses, which - as the name implies - are one-time. As for higher wage pressures, well... just wait until October when everything reverses, Uncle Sam is no longer a better paying competitor to the US private sector, and wages slump.

What does that mean for the economy? Well, all those producers and retailers who got used to bumper demand and pushed their prices sharply and not so sharply higher, will face a stark choice: either drag prices right back down, or sell far fewer goods and services. That, or just await the next bailout.

One thing is certain: six months from today, the US economy will be far, far uglier.

States and cities in the U.S. are cracking down on a niche in house-flipping known as wholesaling conducted by a flood of largely unlicensed middlemen lured in by YouTube tutorials and a torrid market.

Bearing fast cash, wholesalers can help distressed homeowners sell quickly, but have been accused of strong-arm tactics and misinformation. Unlike fix-and-flip investors, who take title to homes, renovate them and put them back on the market, wholesalers typically negotiate with homeowners just to put homes under contract and sell those contracts to flippers.

“I don’t buy houses. I solve problems,” said Scott Sekulow, who leads an Atlanta-area congregation of messianic Jews and bills himself as the Flipping Rabbi. He said clients come his way when they’re going through a divorce, can’t afford massive home repairs or run into other trouble. Sekulow said he can get them cash while also beautifying a neighborhood.

Hedge funds are paying top dollar for the contracts, he told a conference of prospective moguls: “When you can get in with them, they’re there paying stupid money.”

While the practice is legal when transparent, advocates for the poor say aggressive wholesalers dupe sellers with lowball offers. Illinois, Oklahoma, Arkansas, Kansas and the city of Philadelphia proposed or passed regulations recently after complaints. The latter city acted in the fall after neighborhoods were overrun with “We Buy Houses” signs, and reports that hard-charging wholesalers wouldn’t leave houses without a signed contract.

“In my neighborhood in West Philly, I probably get three postcards a month from one of these guys,” said Michael Froehlich, an attorney with Community Legal Services of Philadelphia. “If you can get leads, you can dupe somebody into signing a contract for far less than fair-market value, and you can make $30,000, $40,000, $50,000 on a house.”

The wholesalers, typically entry-level investors who find off-market homes through cold calls or driving through neighborhoods, have been enabled by pandemic-era low interest rates and tight housing supply that have created record price appreciation.

The U.S. had only a 2.4-month supply of unsold houses in April, near a historic low. Prices make many unprofitable for investors, driving some wholesalers to scour working-class and poor neighborhoods to scare up deals. Fees for gathering contracts often run 10% or 15% of the sale price and can generate the wholesaler a $15,000 payday in weeks.

On a recent Monday night in Roswell, Georgia, around 50 wholesalers, flippers and investing neophytes turned out at a DoubleTree hotel for a meeting of the Atlanta Real Estate Investors Alliance. Sekulow, whose brother Jay was one of Donald Trump’s impeachment lawyers, was one panelist.

A second, Mike Cherwenka, calls himself the “Godfather of Wholesaling” and shares testimony on his website of performing in a male revue dance team. He left the life after embracing Jesus and beginning a real-estate career.

“Cash is king, and when you can just offer people cash and close within a week, you’ve got leverage, right?” said Cherwenka, still a muscular figure in a violet-hued sport coat. “People perk up and listen when you make an offer and you’ve got proof of funds right there.”

As discussion turned to the benefits of having a spouse involved in one’s real-estate business, Cherwenka’s wife, Tolla, used a game-show flourish to show off the couple’s book, “The Art of Becoming a Multimillionaire Real Estate Investor.”

“If you’d like one, it’s $20,” he says. “Hold one up there, babycakes.”

Wholesaling has been around for years, but hit the radar of real-estate data provider PropStream in a bigger way four years ago, said Rob Zahr, chief executive of parent company EquiMine in Orange County, California. PropStream’s database can help find homes that are abandoned, at risk of foreclosure or loaded with liens.

A single enthusiastically titled Facebook group -- Wholesaling Houses with PropStream! -- counts more than 41,000 members.

The “low-hanging fruit” of houses that just need a little upgrading are all gone, said Brian Dally, whose Atlanta-based finance company, Groundfloor, expects to fund up to $350 million in real-estate investments this year. What remain aren’t on listing services and need major overhauls.

“You need more scouts out there,” he said. About 40% of the company’s deals involve wholesalers.

Complaints, though, started mounting at legal aid societies for the poor as people flooded into the industry. Because wholesalers often don’t hold real-estate licenses, regulators have had little power. Wholesalers argue they don’t need a license, because they’re buying directly from homeowners, and laws generally permit “for-sale-by-owner” transactions.

In Philadelphia, Froehlich said he heard complaints of wholesalers using a bad news-good news approach on homeowners. The bad news is that a house needs tens of thousands in repairs. The good news is the wholesaler will take it off their hands for $30,000, though it’s really worth $100,000.

Philadelphia last fall created a license for wholesalers and requires them to tell owners how they can obtain fair-market value.

The Oklahoma Real Estate Commission heard about deals that collapsed, clouding the owner’s title, said Executive Director Grant Cody. In other cases, homeowners felt duped upon learning the wholesaler quickly sold the contract.

“It’s kind of like telling your girlfriend, ‘Hey, I want to marry you,’ and then she learns that you just got paid to hand her off to some other guy,” Cody said.

Oklahoma this spring required wholesalers to get a license and allowed the commission to set rules, Cody said. Arkansas and Illinois passed laws in 2017 and 2019, respectively, increasing their power to regulate wholesaling. A bill in Kansas died, but may be reintroduced.

Wholesalers acknowledge they have some bad actors, but say most are genuinely interested in revitalizing housing.

In Atlanta, Duane Alexander, a 37-year-old who jumped into wholesaling during last year’s Covid-19 quarantines, wakes each morning to cold call homeowners. By 10 a.m., he switches to his day job as a software engineer.

So far, Alexander has done four deals, in one case offering $120,000 for a home owned by a friend’s relative and assigning the contract to another investor for $130,000. Alexander made $10,000 for around 10 hours of work.

He said he sees his role as ensuring homeowners get a fair deal and that something nicer rises in a dilapidated home’s place.

“If I know that gentrification is going to happen regardless, as a person who comes from these kinds of neighborhoods, I would rather it be someone like me making money than some hedge fund,” said Alexander.