New York during the inflationary surge of the late 70s and early 80s was a mythical place where one could purchase a Park avenue duplex for $1 (and assume the debt, of course). Now, thanks to the brutal bear hug of the highest interest rates in 40 years and the ongoing CRE crisis, those legendary days have made a comeback to the Big Apple, if only in the realm of commercial real estate for now.

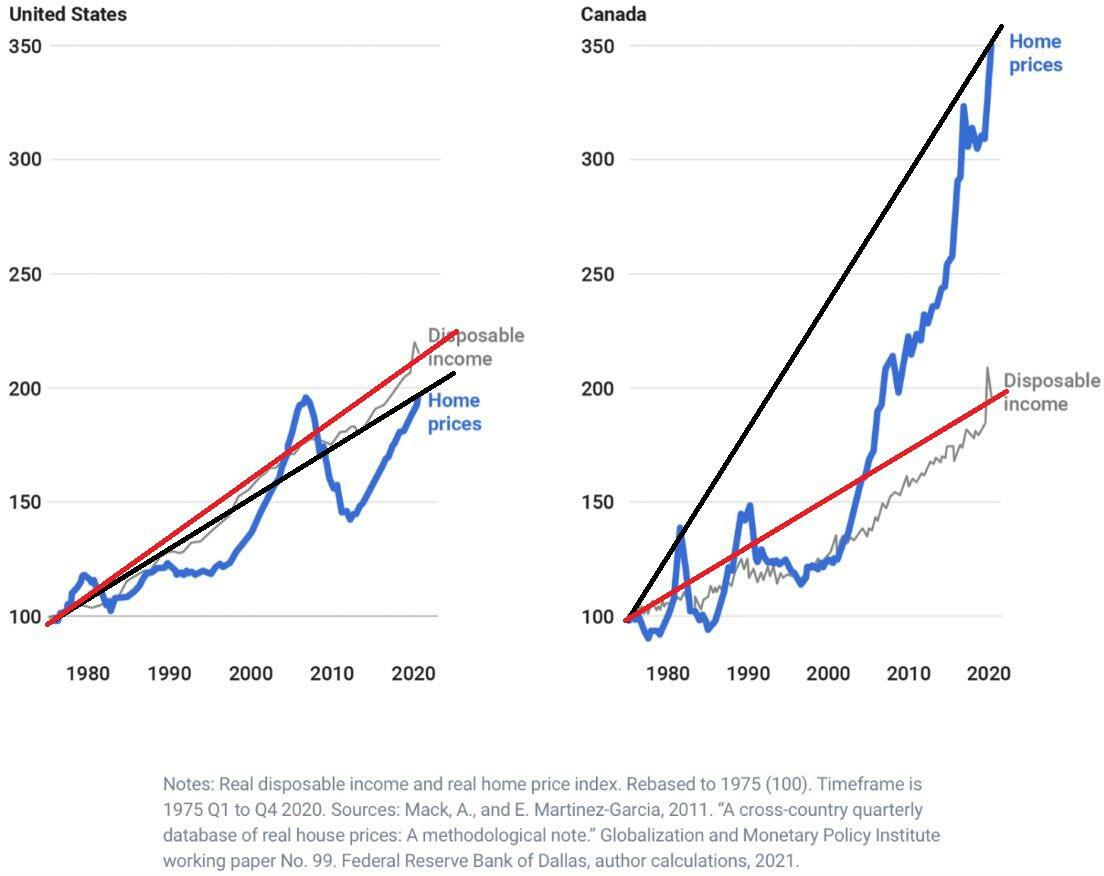

According to Bloomberg, Canadian pension funds - which until recently had been among the world’s most prolific buyers of real estate, starting a revolution that inspired retirement plans around the globe to emulate them, because apparently unlike in the US, Canadian real estate prices never go down...

Freddie Mac reports that the multi-family serious delinquency rate increased sharply in January to 0.44% from 0.28% in December, and up from 0.12% in January 2023.

This graph shows the Freddie multi-family serious delinquency rate since 2012.

Americans are holding on to their homes twice as long as they did 20 years ago, with older generations finding fewer motivations to sell and move, according to a new report.

The average US homeowner has spent just short of 12 years in their home, up from 6½ years two decades ago, according to real estate brokerage Redfin. While the time homeowners stay put has fallen from the 2020 peak of almost 14 years, many incentives motivating folks to move have since flattened.

Other economic indicators suggest as much: US existing home sales hit a 30-year low last year, according to the National Association of Realtors, as homeowners remained locked in by their lower mortgage rates.

The trend was most prevalent among baby boomers, many of whom are retiring asboth rates and home prices remain elevated. The lock-in effect is geographically widespread, with just a handful of affordable metros seeing homes change hands after barely seven years.

"The lock-in effect is … a significant issue among people who say they want to stay in their house longer than they expected," Mark Palim, vice president and deputy chief economist at Fannie Mae, told Yahoo Finance. "We’re not sure that there’s a magical inflection point; we think it’s more than passage of time and rates themselves."

Nearly half of boomers live in homes 20 years

Most baby boomers haven’t moved for decades, and that won't change anytime soon.

Nearly 40% of those born between 1946 and 1964 have lived in their homes for at least 20 years. Another 16% have been in their properties for 10 to 19 years, Redfin found.

For Gen Xers, more than one-third have lived in the same home for at least 10 years.

By comparison, millennials stayed in their homes for shorter periods, largely because they were more likely to switch jobs or have growing families than older generations.

According to Redfin, less than 7% of millennials — those born between 1981 and 1996 — have lived in their home for 10 years or longer, and 30% have lived in their home less than five years.

A handyman-turned-squatter hunter is concerned that migrants entering the U.S. will catch on to states’ lenient tenants’ rights laws and create a squatting crisis that’s “beyond control.”

“We have masses coming in. They’re going to be looking for places to live. And if we don’t have the housing for them, if they’re coming in with no money, they can’t rent the traditional way,” Flash Shelton, founder of the United Handyman Association and SquatterHunters.com, told Fox News.

When they start finding out that many states have permissive laws for squatters, “our squatter situation is going to go beyond control,” he added.

Squatters and tenants’ rights laws vary across the country, with some states providing protection for non-paying individuals, allowing them to occupy a property for extended periods.

In areas where complex laws bar police from taking action, homeowners have few options to reclaim their property beyond pursuing a civil case, which can take months.

Shelton has advocated for reforming laws to hamper people’s ability to squat and warned that the influx of migrants coming across the southern border could make the squatting problem substantially worse.

Flash Shelton, founder of the United Handyman Association and SquatterHunters.com.FOX News

“What are we going to do later when we have a million people squatting in this country,” Shelton said, “when not only do we have a border issue that we can’t even figure out, but now we have people that are being mentally, financially, physically messed with because they’ve lost their home to all of these people?”

“Regardless of how you feel politically or morally about the situation, put that aside and just think about the masses,” Shelton added.

Nearly 7.3 million migrants have crossed into the U.S. illegally since the start of 2021, according to U.S. Customs and Border Protection (CBP). Since 2022, Texas has sent over 100,000 migrants to major cities in other states, with most ending up in New York City and Chicago.

The Big Apple spent $1.45 billion in fiscal 2023 on migrant costs and expects to spend a combined $9.1 billion housing migrants in 2024 and 2025, according to Bloomberg.

Squatting crisis will be ‘beyond control’ if laws don’t change, the handyman said.FOX News

“Let me tell you something New Yorkers, never in my life have I had a problem that I did not see an ending to — I don’t see an ending to this,” New York City Mayor Eric Adams said in September. “This issue will destroy New York City.”

The already lacking resources to handle the hundreds of thousands of homeless Americans living on city streets across the country have been further depleted due to the new flood of people seeking refuge, Shelton said. He questioned what’s to stop migrants from using squatting loopholes to their advantage if they realize they can reside in vacant homes rent-free for months on end.

“We have irresponsibly opened a door for a whole lot of people to come into this country, and we aren’t prepared to deal with them,” Shelton said. “What’s the negative for these people to then start taking over these houses?”

New York City Mayor Adams said he “doesn’t see an ending” to this problem.FOX News

The California handyman had his first experience removing squatters in 2019 when two women took over his mother’s home that was up for sale.

After local law enforcement couldn’t help, Shelton spent days dissecting laws around squatters’ rights and managed to get rid of the women within a day using a loophole that included signing a lease agreement with his mother designating him as the legal resident of the home. Now he uses his experience to provide squatter removal services for others.

He warned about the “nightmare scenario” the country will face down the road if politicians don’t take action to curb squatting now.

“I’m spending all this time trying to bring awareness to squatting and bring awareness to how the law needs to change,” Shelton told Fox News. “Is it going to get worse before it gets better? I think it’s already there.”

“I think it’s going to just get beyond repair at some point,” he added.

Families with kids are being boxed out of the increasinglyunaffordable US housing market as the cost of both a new mortgage and child care soar higher.

A recent study published by Zillow found that potential homebuyers with children are likely to spend 66% of their income on monthly mortgage payments and child care, a sharp increase from about 50% in 2019.

The typical American family can expect to spend about $1,984 per month on child care and $1,973 on a monthly mortgage payment (based on an interest rate of 6.6%).

With the monthly median household income hovering around $6,640, that leaves just $2,683 for other necessary expenses, including food, health care, insurance, transportation, retirement savings and education.

The general rule of thumb is that housing should cost no more than 30% of a person’s monthly income, while the Department of Health and Human Services recommends that families spend no more than 7% of their income on child care expenses.

A recent study found that potential homebuyers with children will spend 66% of their income on monthly mortgage payments and child care.Getty Images

In fact, in 31 of the largest 50 metropolitan areas with available child care cost data, families looking to buy a home can expect to spend more than 60% of their income on their mortgage and child care expenses.

The cost burden is even worse in some parts of the country.

Parents in Los Angeles and San Diego would need to dedicate a respective 121% and 113% of their income to pay for child care and a mortgage. In both Boston and Seattle, families would need to spend 92%.

Housing affordability is the worst it’s been in decades, thanks to a spike in home prices and mortgage rates.

Combined, the two have helped to push the typical portion of average wages nationwide required for major homeownership expenses up to 33%.

There are several reasons to blame for the affordability crisis.

The Federal Reserve’s aggressive interest-rate hike campaign sent mortgage rates soaring above 8% for the first time in nearly two decades last year.

Rates have been slow to retreat, hovering near 7% as hotter-than-expected inflation data dashed investors’ hopes for immediate rate cuts.

The average rate for a 30-year fixed loan rose to 6.77% last week, Freddie Mac reported, well above the pandemic-era lows of 3%.

Even thoughmortgage rates are nearly double what they were three years ago, home prices have hardly budged.

That is largely due to a lack of available homes for sale. Sellers who locked in a low mortgage rate before the pandemic began have been reluctant to sell, leaving few options for eager would-be buyers.

“This rapid home price appreciation, coupled with mortgage rates that recently hit decades-long highs, means many home buyers must make trade-offs in order to afford other necessary expenses, such as child care,” the Zillow analysis said.

Democrat politicians in cities such as New York, often criticized for their disastrous progressive policies, have transformed the metro area into what some believe is a 'hellhole,' overrun by violent crime, migrants, homelessness, open-air drug markets, and constant chaos. According to one real estate investor with a commercial real estate portfolio worth billions of dollars, Democrats are quickly transforming NYC's CRE market into an unattractive option for investment.

On X this week, real estate investor and influencer Grant Gardone said his real estate team at Cardone Capital has "Immediately discontinued ALL underwriting on New York City real estate."

"The risk outweigh the opportunities at this time. Recent political decisions will continue to deteriorate price and benefit states that don't have these challenges," Gardone said.

He told his real estate team to concentrate on "Texas & Florida" markets where the political environment is not hostile, and overall state economies are friendly towards investors.

"Why would I buy in New York City where you can't actually collect rent, taxes are higher, & illegals are treated better than property owners," Cardone wrote in a post last month.

Adding this...

And the investor pointed out on X, "This NYC Judge will sell more real estate in Florida than all the real estate agents & broker's combined."

Cardone Capital's website says it manages a real estate portfolio with more than 500,000 square feet of CRE office space and 11,903 apartment units valued at approximately $4 billion.

"We invest for 14,000 investors at Cardone Capital that depend on cash flow. And if I can't predict the cash flow because of some ruling, or because of the migrants, or because I can't evict people, New York City just keeps doing every single thing they can to sell real estate in Florida, not sell real estate in New York," the investor said in a Fox News interview on Wednesday.

Meanwhile, O'Leary Ventures chief Kevin O'Leary echoed a similar warning:

"New York was already a loser state, like California is a loser state. I would never invest in New York now. And I'm not the only person saying that," O'Leary said.

Furthermore, in the Federal Reserve's last meeting, the minutes from the session, published on Wednesday, showed the CRE downturn is only gaining steam:

CRE prices continued to decline, especially in the multifamily and office sectors, and low levels of transactions in the office sector likely indicated that prices had not yet fully reflected the sector’s weaker fundamentals.

The minutes noted:

Leverage in the financial sector was characterized as notable. In the banking sector, regulatory risk-based capital ratios continued to increase and indicated ample loss-bearing capacity in the banking system.

And also this:

The staff provided an update on its assessment of the stability of the U.S. financial system and, on balance, characterized the system’s financial vulnerabilities as notable. The staff judged that asset valuation pressures remained notable, as valuations across a range of markets appeared high relative to fundamentals

Back to NYC's CRE market - well done, Democrats. The blowback wave from your failures is accelerating in a market that only points down.