Churches across the US are working with homeless charities to construct tiny home communities amid one of the worst housing affordability crises ever.

AP News says churches are using spare land to build tiny home communities to accommodate the homeless.

On vacant plots near their parking lots and steepled sanctuaries, congregations are building everything from fixed and fully contained micro homes to petite, moveable cabins, and several other styles of small-footprint dwellings in between.

Church leaders are not just trying to be more neighborly. The drive to provide shelter is rooted in their beliefs — they must care for the vulnerable, especially those without homes. -AP

More than half a million Americans were homeless in 2020, and the number has likely climbed as shelter costs if renting or owning have exploded, triggering the worst ever housing affordability crisis on record. As we've previously noted, soaring shelter costs force people into homelessness.

Days ago, we outlined how a tidal wave of evictions could be ahead with 8.4 million Americans, or about 15% of all renters were behind rent payments. Of that, 3.5 million said they could be evicted within the next two months. Unlike the pandemic, the federal eviction moratorium prevented people from ending up on the streets, though the moratorium has since expired during the worst inflation storm in four decades.

Jeff O'Rourke, lead pastor of Mosaic Christian Community in St. Paul, Minnesota, embraced tiny homes as a housing solution. He said his church uses "every square inch of property that we have to be hospitable."

Meridian Baptist Church in El Cajon, California, partnered with local nonprofit Amikas to construct a tiny home community to address the homelessness crisis.

In the San Francisco Bay Area, Firm Foundation Community Housing, launched by Rev. Jake Medcalf, has erected a tiny home housing community in the parking lot of First Presbyterian Church of Hayward.

The First Christian Church of Tacoma in Washington erected an entire village of tiny homes in their parking lot.

"We don't have a lot of money. We don't have a whole lot of people … but we care a lot about it, and we've got this piece of property," said the Rev. Doug Collins, the church's senior minister.

Donald Whitehead, director of the National Coalition for the Homeless, told AP the move by churches across the country to build tiny home communities is a "great emergency option" amid today's economy that hasn't worked for everyone.

Maybe all of these tiny home communities springing up at US churches should be dubbed "Bidenvilles," similar to the shacktowns built during the Great Depression in the 1930s called "Hoovervilles."

“Requests to transfer a co-op’s shares to a trust or to buy a co-op with a trust or limited liability company do add another layer of bureaucracy for a co-op—but an increasing number of boards are considering it,” says James Woods, Esq., managing partner at Woods Lonergan PLLC,a Manhattan-based law firm focused on real estate and in particular, cooperative board representation as well as buyers and sellers.

In many cases, shareholders are pushing boards to allow the transfer of shares to a trust for estate planning reasons or because it often entitles the grantor to tax benefits.

Allowing trusts may also make the co-op more desirable, opening up the buyer pool in the case of trust purchases. Permitting trust transfers can also be a way to raise revenue for the building if the governing documents allow fees to be levied when shares are transferred.

What are the risks of allowing trust purchases or transfers to a trust?

Trusts have an opaque ownership structure, making it more complicated to go after an individual shareholder if the maintenance or assessments are not paid.

“Without adequate protection, the co-op board can’t turn to the occupant of the apartment in order to address a default and you could have problems with unauthorized occupants in the apartment,” Tobin says.

Another concern might be the question of which individual associated with the trust has co-op voting rights. If there are multiple beneficiaries or trustees claiming voting rights this could result in confusion during an election.

What process should our board follow if we decide to allow trust purchases or transfers to a trust?

You will first need to check the governing documents to see what the co-op allows.

“If a transfer to trust is permitted in the governing documents of the co-op, permitting trust ownership is a good way to accommodate shareholders, but the co-op will want to take protections too,” says Lauren Tobin, Esq., an associate attorney at Woods Lonergan PLLC, specializing in the co-op board, buyer and seller representation.

With the support and oversight of an experienced co-op attorney, the precautions a board takes can prevent some of the headaches that might arise with transfers to trusts and LLCs.

“As a precondition for this type of transaction, the board will want to have a prospective purchaser or shareholder provide a range of documents to be reviewed by the co-op attorney,” Woods says. In addition, you will want the grantor to commit to paying for the trust review process, which might amount to a few thousand dollars.

One important document is an opinion letter from the attorney who originally drafted the trust. “This document outlines who the grantor is, who the trustees and beneficiaries are, and expresses the opinion that the trust was validly formed and the transfer contemplated is permitted by the trust document,” Tobin says.

Some trusts are not formed to hold assets like co-op apartments or were created in other jurisdictions, so an opinion letter from the attorney who drafted the trust is an added protection for the co-op.

“Your co-op attorney will also be an extra set of eyes on the document to make sure the transfer is proper,” she says.

Additionally, an agreement should also be drafted that clearly identifies the authorized occupants of the apartment. “In the case of a transfer, this is often the grantor or the person who currently owns the shares so there might not even be a need for an interview,” Tobin says.

However, you will want to establish at the outset that if there is a beneficiary or occupant who is not the current shareholder, they will need to seek board approval. “They would need to be interviewed in exactly the same way as would a traditional co-op purchaser,” Woods says.

At the closing, you will also want an agreement stating that the occupant personally guarantees the financial obligations under the lease.

“That would mean any default in the maintenance or assessments would be met by the person living in the apartment,” Woods says.

So if, in the worst case scenario, you end up in court, you are not only turning to the trust assets for a remedy but also the person living in the apartment who takes on a financial responsibility if there is a default or other liability.

In most trust transfer or trust purchase situations, Woods says his firm will also require an additional agreement requiring that the board receive written notification of any changes to the trust.

“If there are material changes, or changes to the beneficiaries, or trustees, the board would want to approve those changes as they are in effect, transfers,” he says. The board always needs up to date information on who is the responsible party.

If there are multiple trustees, the board will want to clarify who has voting rights.

“This is another important detail that needs to be squared away at closing before anything is transferred,” Tobin says.

Can board collect flip tax on trust purchases or transfers to trust?

One other consideration for a board is whether or not the building can collect a fee or flip tax when a co-op is transferred to a trust.

“You could have a situation where the occupants change but since the shares are in the name of the trust, the board does not collect a flip tax,” Tobin says. For example, say the occupant passes away or wants to allow another to occupy the apartment, this can be effectuated without any change in ownership. Therefore, the co-op will miss an opportunity to collect a flip tax.

The ability to collect a fee from the transfer of shares to a trust likely will be outlined in the governing documents. In some cases, the transfer of an apartment in a co-op to a direct family member is permitted by the governing documents without incurring a flip tax regardless of whether a trust is involved.

It’s also possible the board will want to consider an amendment to the bylaws allowing the implementation of fees for trusts in order to generate revenue for the building. If you do adopt this type of policy it would need to be applied uniformly to all shareholders.

Freddie Macannounced Wednesday that on-time rental payments will be included in its underwriting system. The government-sponsored enterprise said that it hopes to incentivize “responsible” renters to make a leap into homeownership.

According to Freddie, this option will be available starting July 10 and will allow mortgage lenders to submit a borrower’s bank account data that shows a 12-month streak of on-time rent payments to its automated underwriting system.

Michael DeVito, CEO of Freddie Mac, said in a statement that millions of potential borrowers have been blocked off from homeownership because they lack a credit score, or have a limited credit history.

“By factoring in a borrower’s responsible rent payment history into our automated underwriting system, we can help make home possible for qualified renters, particularly in underserved communities,” DeVito said.

Freddie said in its announcement that a borrower’s bank account data – with a borrower’s permission—can be plucked from apps such as Zelle,Venmo or PayPal. The government- sponsored enterprise added that additional requirements for submitting rent payment data to its underwriting system will be announced sometime in July.

Freddie Mac has been eyeing different ways of incorporating on-time rental payments to help borrowers qualify for a mortgage.

In November 2021, Freddie Mac announced that it wanted to encourage multifamily landlords to report positive rental payments to the credit bureaus to give renters a better shot at qualifying for a mortgage.

The government-sponsored enterprise said at the time that it would provide closing cost credits on multifamily loans for rental landlords who agree to report on-time rental payments through Esusu Financial.

As a result of this initiative, 70,000 households across 816 multifamily properties are enrolled in the program and more than 15,000 credit scores have been established, Freddie said.

Freddie Mac is following in the footsteps of Fannie Mae, which announced in August 2021 that on-time rental payments would factor into its underwriting calculations.

Fannie said that for first-time homebuyers’ a history of consistent rent payments makes a “significant difference” in helping an applicant qualify for a mortgage.

Per its research conducted last year, in a sample of mortgage applicants who were denied a mortgage, 17% could have received an approval if their rental payment history had been considered.

Theaughts are back in style, with early-2000s inspiration trending in fashion, music and mortgage costs.

Housing affordability last month reached its lowest point since at least 2007, according to a recent report from Zillow. That’s as far back as the company’s affordability metric goes.

Housing prices continued their rise, though the growth acceleration finally showed signs of slowing last month. Meanwhile, mortgage rates and payments continue to balloon, while inventory is not recovering quickly enough to ease the supply-demand disparity.

Mortgage rates were flirting with the 6 percent mark last week, mere months after exceeding the 5 percent threshold. The rates are still historically low, but significantly higher than they were in the first couple of years of the pandemic.

As a result, mortgage payments are rocketing. At Thursday’s average rate of 5.78 percent, the mean monthly mortgage payment in the country would be $2,127, according to Zillow. That’s a 51 percent surge year-over-year and a 36 percent increase from the beginning of the year.

In April, monthly mortgage payments took 28 percent of homeowners’ income; 30 percent is considered a cost burden.

There are small glimmers of hope for homebuyers. According to Zillow’s index, price growth in April was 20.9 percent versus 20.7 percent in May. Last month was the first in more than a year to feature a deceleration in price growth, according to Zillow; the S&P CoreLogic Case-Shiller Index for May won’t be out until late next month.

Inventory is also showing signs of recovery. Listings increased 10.5 percent from the previous month in April. Listings are still 14.2 percent below levels from the previous year, though, and 50 percent below the mark of May 2019.

Weary home buyers can’t exactly kick back and turn to the rental market. Rents are shooting up similarly to mortgage payments — May’s annual rent appreciation was 15.9 percent and the typical rent in the country was only a few cups of coffee shy of $2,000; Redfin reported that the benchmark was exceeded last month.

Despite rising rents, mortgage payments exceed monthly rent statements in all but five states. That’s a drastic change from 2019, when rent was higher than mortgage payments in a small majority of states.

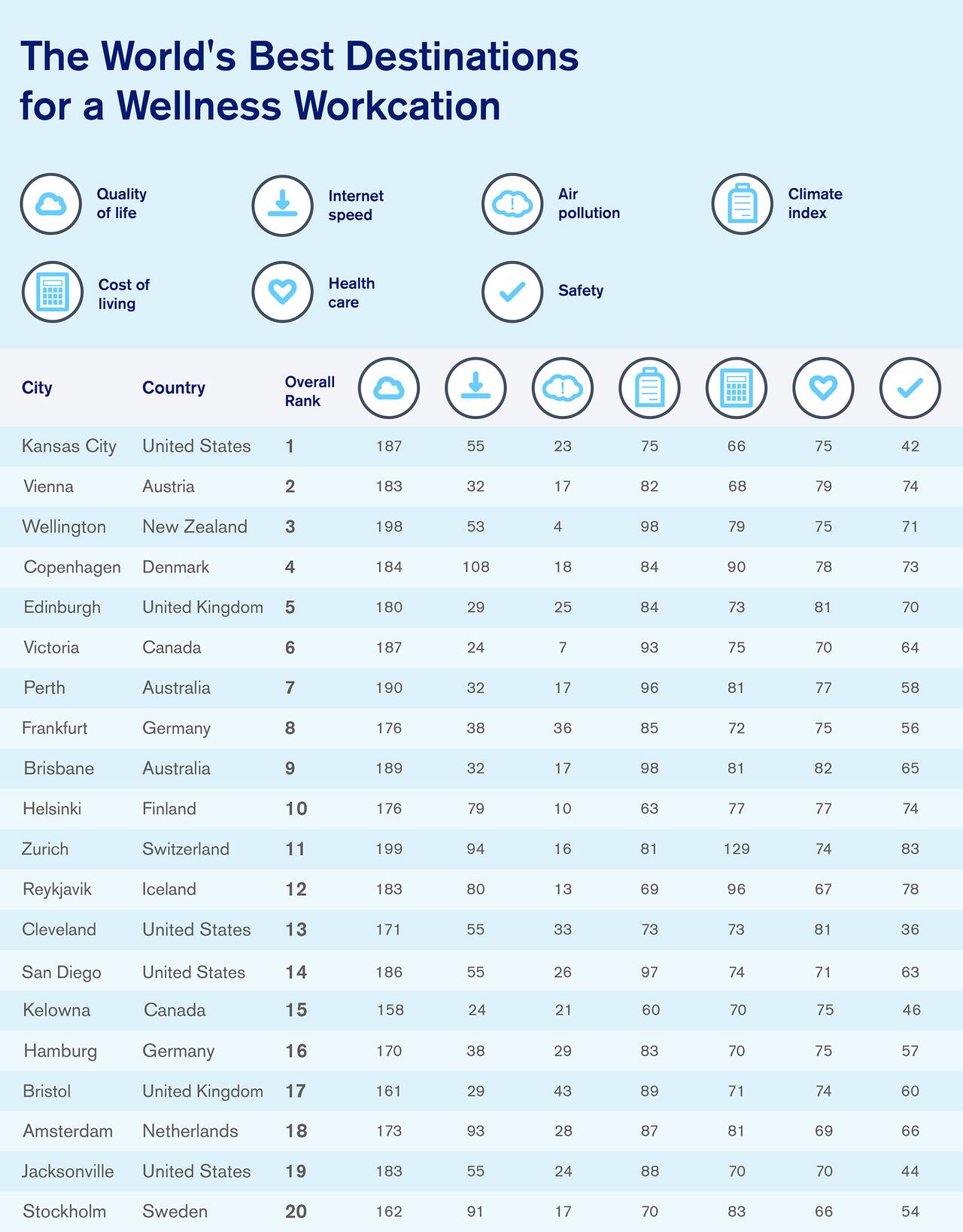

There has always been a clear division between work and play. Yet there's a new travel trend dubbed "workcations," where white-collar workers can remotely work from mountain cabins in Jackson Hole, Wyoming, to a beach resort in Tulum, Mexico, to the jungles of Costa Rica and even large metro areas like Paris, Tokyo, and Miami. Once they're finished work for the day, they explore the outdoors, local food markets, and whatever the nightlife has to offer.

Booking a workcation could be challenging because there are so many factors about a metro area that workers need to be aware of for a productive and fun time.

Icelandair, the top airline carrier in Iceland, commissioned a study examining 150 cities around the world for various factors related to a wellness workcation. They did the heavy lifting and uncovered the best 25 cities globally for remote work while also focusing on the importance of personal wellbeing and acts of self-care.

Icelandair used several factors to determine the top metro areas for a workcation, including quality of life, internet speed, air pollution, cost of living, health care, and safety.

They found that the best city in the world for remote work is one where Americans don't even need a passport, and it's not the beaches of San Diego or the vast forests of Yellowstone National Park, but Kansas City, Missouri.

For those unfamiliar with Kansas City, it's a metro area on Missouri's western edge, straddling the border with the state of Kansas -- known for barbecue, jazz heritage, and fountains. It ranks the highest on Icelandair's factors than any of the 150 cities worldwide that the airline examined.

Vienna, Austria, and Wellington, New Zealand round out the list of the top three metro areas for remote work worldwide.

Everything may be bigger in Texas, but Shaquille O’Neal is opting for a smaller abode when it comes to his next house.

Months after selling his mega-mansion in Orlando, Fla., the NBA legend purchased a much smaller, five-bedroom, six-bathroom estate in the Dallas suburbs.

Located in Carrollton, the final listing price of the home was $1.224 million. But it appears the actual price O’Neal paid for it must have been way above asking. While the final sale price is hush-hush, the previous listing did note that there was a deadline for final offers by April 21 — only three days after it first hit the market.

The competitive housing market means O’Neal likely overpaid for the property significantly. According to the Dallas Morning News, which was the first to report the transaction, O’Neal’s expansion of his Big Chicken restaurant chain in Texas was a factor in the purchase.

“It has a lot to do with that, and basic travel — he travels here quite a bit for different things,” Zac Gideo, a real estate agent for Rogers Healy, who worked O’Neal to buy the home, told the outlet. adding that the star plans on living here part-time.

The home spans over 5,200 square feet.James Davis of Better Angle MediaThe great room with a wall of windows.James Davis of Better Angle MediaThe gourmet kitchen.James Davis of Better Angle MediaThe library/study with a wood-burning fireplace.James Davis of Better Angle MediaThe movie theater.James Davis of Better Angle MediaThe primary suite.James Davis of Better Angle Media

Spanning over 5,200 square feet, features include a library with a dramatic tiered ceiling, a wall of built-in shelves, and a wood-burning fireplace. The kitchen and breakfast room opens out to the great room that offers soaring ceilings, a gas fireplace and a wall of windows overlooking the pool.

The primary suite features a sitting area with a spa-like bathroom, according the listing.

But to compare, his Orlando place, which he finally sold after three years on the market, spanned a colossal 31,000 square feet and had 12 bedrooms and 11 bathrooms. It even came with a full-sized basketball court with a 6,000 square-foot “Shaq Center” with bleachers.

The primary bathroom.James Davis of Better Angle MediaOne of five bedrooms.James Davis of Better Angle MediaThe fitness room.James Davis of Better Angle MediaThe home is surrounded by lush trees.James Davis of Better Angle MediThe covered patio.James Davis of Better Angle MediaThe pool and spa.James Davis of Better Angle Media

Outdoor amenities of his new home include the large pool with an attached spa and a rock waterfall and an awning-covered patio.

Cindy O’Gorman with Ebby Halliday – North Dallas held the listing.

As costs of home ownership rise, millions of Americans have been pushed out of the housing market, according to Harvard University’s annual State of the Nation’s Housing Report released Wednesday.

At today’s home prices, a first-time buyer would have had to shell out $27,400 (7 percent of the sales price) as a down-payment in April on a median-priced home, said the report. This rules out 92 percent of renters, who only have a median of $1,500 in savings. If the downpayment is halved to 3.5 percent, the monthly mortgage payment on a median-priced home would be $2,020.

“In combination with rising prices, the recent interest rate hikes raised the minimum income needed to afford these payments from $79,600 in April 2021 to $107,600 in April 2022 - effectively pricing out some 4 million renter households with incomes in this range,” the report said.

Between December 2021 and mid-April 2022, mortgage interest rates rose by 2 percent, which is equivalent to a 27 percent jump in home prices. As prices increased along with interest rates, the income and savings required to qualify for a home loan “skyrocketed.” This presents a financial burden on middle-income and first-time buyers.

In April 2021, the interest rate was at 3.06 percent, growing to 4.98 percent by April 2022. During this period, the value of a median-priced home jumped from $340,700 to $391,200.

The down-payment and closing costs, which came in at $22,100 in April last year, rose to $25,400 this April. Monthly mortgage payments rose from $1,400 to $2,020 while total monthly owner costs jumped from $2,060 to $2,780.

Persistently Soaring Prices

Home price appreciation across the United States hit 20.6 percent in March 2022, eclipsing the previous high of 20 percent in August 2021. This was also the largest jump in three decades.

“The runup has been widespread, with 67 of the top 100 housing markets experiencing record-high appreciation rates at some point over the past year. And even in the other 33 major markets, home prices increased by at least 9 percent,” the report states.

A recent Goldman Sachs note says the company expects houses to become much less affordable for average Americans despite home price growth slowing down sharply, according to Business Insider. An average American is now much less likely to be able to afford a home when compared to just a few months ago.

“In the US, our latest model update pointed to substantial slowing in home price growth to the low single digits over the next year,” Goldman analysts wrote. Since the COVID-19 pandemic began, U.S. home prices have risen by around 38 percent according to the Case-Shiller Home Price Index.

Here is a table of selected public builders and the currently reported cancellation rate (I’m still gathering data). There is some seasonality to cancellation rates. The only builder that reported a sharp increase recently was KB Home comparing the three months ended May 31, 2022, with the three months ended May 31, 2021.

“The cancellation rate as a percentage of gross orders was 17%, compared to 9%.”

However, as KB Home noted on their conference call yesterday, a large portion of the increase in cancellations were on “unstarted homes”. ... Currently cancellation rates are below normal for the home builders. As an example, Toll Brothers recently announced a cancellation rate of 3.8%, down from 4.3% the previous quarter, and well below their historical rate of 7%. During the housing bust, Toll Brothers cancellation rates peaked close to 40%.

Realtor.comhas monthly and weekly data on the existing home market. Here is their weekly report released yesterday from Chief Economist Danielle Hale:Weekly Housing Trends View — Data Week Ending June 18, 2022. Note: They have data on list prices, new listings and more, but this focus is on inventory.

• New listings–a measure of sellers putting homes up for sale–were up 6% above one year ago. Home sellers in many markets across the country continue to benefit from rising home prices and fast-selling homes. That’s prompted a growing number of homeowners to sell homes this year compared to last, giving home shoppers much needed options. We’ve seen more homes come up for sale this year compared to last year in 11 of the last 12 weeks.

• Active inventory continued to grow, rising 21% above one year ago. Inventory was roughly even with last year’s levels at the beginning of May and the gains have mounted each week. Still, our May Housing Trends Report showed that the active listings count remained nearly 50 percent below its level at the beginning of the pandemic. In other words, we’re starting to add more options, but the market needs even more before home shoppers have a selection that’s roughly equivalent to the pre-pandemic housing market.

Here is a graph of the year-over-year change in inventory according to realtor.com.

Note the rapid increase in the YoY change, from down 30% at the beginning of the year, to up 21% YoY now. It will be important to watch if that trend continues.

Nationwide Home-Flipping Rate Jumps to Highest Level This Century; Raw Profits on Home Flips Increase for First Time Since 2020; But Typical Profit Margins on Flips Decline Again, to Lowest Point Since 2009

ATTOM, a leading curator ofreal estate datanationwide for land and property data, today released its first-quarter 2022 U.S. Home Flipping Report showing that 114,706 single-family houses and condominiums in the United States were flipped in the first quarter. Those transactions represented 9.6 percent of all home sales in the first quarter of 2022, or one in 10 transactions – the highest level since at least 2000. The latest total was up from 6.9 percent, or one in every 14 home sales in the nation during the fourth quarter of 2021, and from 4.9 percent, or one in 20 sales, in the first quarter of last year.

The jump in the home-flipping rate during the first quarter of this year marked the fifth straight quarterly increase. It also represented the largest quarterly and annual percentage-point gains since 2000.

But the report also shows that as home sales by investors spiked, typical raw profits on those deals remained below where they were a year ago, and in a more striking trend, profit margins dipped to their lowest point since 2009.

“The good news for fix-and-flip investors is that demand remains strong from prospective homebuyers, as evidenced by this quarter’s report, which shows that one of every 10 homes sold during Q1 was a flip,” said Rick Sharga, executive vice president of market intelligence for ATTOM. “The bad news is that rising mortgage interest rates are beginning to slow down home price appreciation rates, and buyers have become more selective – and less willing to outbid other buyers for properties they’re interested in. This is having a predictable impact on profit margins for investors.”

Among all flips nationwide, the gross profit on typical transactions (the difference between the median purchase price paid by investors and the median resale price) stood at $67,000 in the first quarter of 2022. While that was up 5.5 percent from $63,500 in the fourth quarter of 2021, and represented the first increase since late 2020, it was 4.3 percent less than the $70,000 level recorded in the first quarter of 2021.

Profit margins, meanwhile, fell for the sixth quarter in a row, as the typical gross-flipping profit of $67,000 in the first quarter of 2022 translated into just a 25.8 percent return on investment compared to the original acquisition price. The national gross-flipping ROI was down from 27.3 percent in the fourth quarter of 2021 and from 38.9 percent a year earlier. It sat at the lowest point since the first quarter of 2009, when the housing market was slumping from the effects of the Great Recession in the late 2000s.

The latest return on investment also was less than half the peak of 53.1 percent for this century, which hit in late 2016.

Profit margins declined in the first quarter of 2022 as resale prices on flipped homes continued to shoot up more slowly than they were when investors originally bought their properties.

Specifically, the median price of homes flipped in the first quarter of 2022 increased to another all-time high of $327,000. That was up 10.5 percent from $296,000 in the fourth quarter of 2021 and 30.8 percent from $250,000 a year earlier. Both increases stood out as the largest for flipped properties since 2000.

Home flipping rates up in 95 percent of local markets

Home flips as a portion of all home sales increased from the fourth quarter of 2021 to the first quarter of 2022 in 181 of the 191 metropolitan statistical areas around the U.S. analyzed for this report (95 percent). Rates went up quarterly by at least two percentage points in 99 of those metros (52 percent). (Metro areas were included if they had a population of 200,000 or more and at least 50 home flips in the first quarter of 2022.)

Among those metros, the largest flipping rates during the first quarter of 2022 were in Phoenix, AZ (flips comprised 18.7 percent of all home sales); Charlotte, NC (18 percent); Tucson, AZ (16.2 percent); Atlanta, GA (16.1 percent) and Jacksonville, FL (16 percent).

The highest flipping rates during the first quarter of 2022 in metro areas with a population of less than 1 million were in Durham, NC (15.3 percent); Gainesville, FL (14.9 percent); Ogden, UT (13.9 percent); Clarksville, TN (13.4 percent) and Winston-Salem, NC (13.4 percent).

The smallest home-flipping rates among metro areas analyzed in the first quarter were in Olympia, WA (4.4 percent); Portland, ME (4.6 percent); Salem, OR (4.7 percent); Syracuse, NY (4.7 percent) and Davenport, IA (4.9 percent).

Typical home flipping returns decrease in three quarters of metro areas

The median $327,000 resale price of homes flipped nationwide in the first quarter of 2022 generated a gross flipping profit of $67,000 above the median investor purchase price of $260,000. That resulted in a 25.8 percent profit margin.

Profit margins dipped from the first quarter of 2021 to the first quarter of 2022 in 139 of the 191 metro areas with enough data to analyze (73 percent).

The biggest annual declines came in Salisbury, MD (ROI down from 173.7 percent in the first quarter of 2021 to 29.3 percent in the first quarter of 2022); Elkhart, IN (down from 148.3 percent to 24.9 percent); Macon, GA (down from 120.7 percent to 50.9 percent); Lynchburg, VA (down from 96.2 percent to 31.5 percent) and Flint, MI (down from 126.2 percent to 64 percent).

Markets with the largest returns on investment during the first quarter of 2022 on typical home flips were Scranton, PA (115.5 percent); Kingsport, TN (114 percent); Reading, PA (108.6 percent); Pittsburgh, PA (105.7 percent) and Johnson City, TN (101.1 percent).

Aside from Pittsburgh, the largest investment returns in the first quarter among metro areas with a population of at least 1 million were in Buffalo, NY (ROI of 88.2 percent); Philadelphia, PA (80.3 percent); Richmond, VA (79 percent) and New Orleans, LA (69.9 percent).

Metro areas with the smallest profit margins on typical home flips in the first quarter of 2022 were Boise, ID (4.4 percent return); Fort Collins, CO (5.7 percent); College Station, TX (7.2 percent); Sacramento, CA (9 percent) and Santa Rosa, CA (9.6 percent).

West and Northeast continue to boast largest raw profits; South and Midwest have smallest

The highest raw profits on median-priced home flips in the first quarter of 2022, measured in dollars, were concentrated among western and northeastern metro areas. Twelve of the top 15 were in those regions, led by San Jose, CA (typical gross profit of $420,000); San Francisco, CA ($220,000); Seattle, WA ($155,000); Bremerton, WA ($150,000); and Naples, FL ($145,000).

At the opposite end of the range, 20 of the 25 lowest raw profits on typical home flips were spread across the South and Midwest. The smallest were in Syracuse, NY ($16,687 profit); Boise, ID ($18,662); Lubbock, TX ($19,057), College Station, TX ($19,833) and Amarillo, TX ($20,875).

Almost two-thirds of flipped homes purchased with cash by investors

Nationwide, 62.7 percent of homes flipped in the first quarter of 2022 had been purchased by investors with cash. That figure was virtually unchanged from 62.9 percent in the fourth quarter of 2021, but up from 60.9 percent in the first quarter of 2021. Meanwhile, 37.3 percent of homes flipped in the first quarter of 2022 had been bought with financing. That was about the same as the 37.1 percent portion in the prior quarter, but down from 39.1 percent a year earlier.

“As interest rates continue to go up, cash buyers should be in an even greater position of competitive advantage in the fix-and-flip market,” Sharga noted. “It will be interesting to see if the percentage of cash purchases, and purchases made by larger, better capitalized investors, increases over the next few quarters.”

Among metropolitan areas with a population of 1 million or more and sufficient data to analyze, those with the highest percentage of flips in the first quarter of 2022 that had been purchased with cash were in Buffalo, NY (86.4 percent); Detroit, MI (84 percent); Tucson, AZ (78.1 percent); Cincinnati, OH (76.5 percent) and Raleigh, NC (76.5 percent)

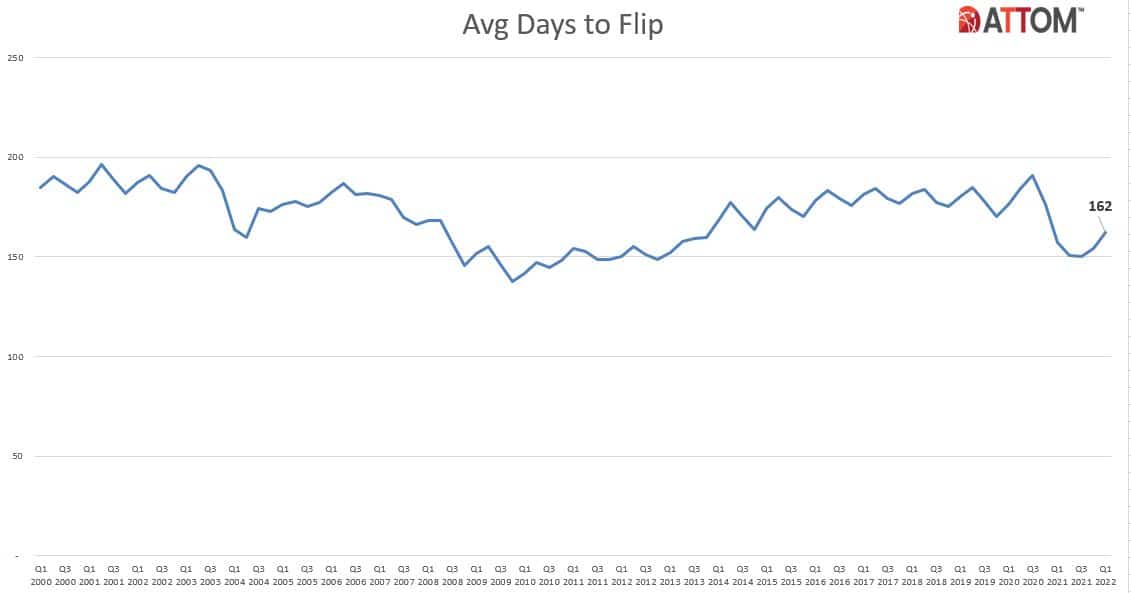

Average time to flip nationwide rises slightly

Home flippers who sold properties in the first quarter of 2022 took an average of 162 days to complete the transactions. While that was less the historical averages, it was still up from an average of 154 in the fourth quarter of 2021 and 157 in the first quarter of 2021.

Investor resales to FHA buyers remain low

Of the 114,706 U.S. homes flipped in the first quarter of 2022, only 7.9 percent were sold to buyers using loans backed by the Federal Housing Administration (FHA). That was down slightly from 8 percent in the prior quarter and down from 9.5 percent in the first quarter of 2021, to the third-lowest quarterly mark since 2007.

Among the 191 metro areas with a population of at least 200,000 and at least 50 home flips in the first quarter of 2022, those with the highest percentage of flipped properties sold to FHA buyers — typically first-time home purchasers — were Visalia, CA (26.6 percent); Lake Charles, LA (23.2 percent); Springfield, MA (22.2 percent); Hagerstown, MD (22.2 percent) and Yuma, AZ (21.7 percent).