ATTOM, a leading curator of real estate data nationwide for land and property data, today released its year-end 2021 U.S. Home Flipping Report, which shows that 323,465 single-family homes and condos in the United States were flipped in 2021. That was up 26 percent from 2020, to the highest point since 2006.

The report reveals that the number of home flips in 2021 was up from 257,091 in 2020 to a total not seen since nearly 334,000 homes were flipped by investors in 2006. Last year’s flips represented 5.5 percent of all home sales in the nation during 2021, down from 5.8 percent in 2020 and 6.1 percent in 2019.

But even as quick-turnaround sales by investors shot up, gross profit margins on home flips in 2021 sank to their lowest level in more than a decade after dropping at the fastest pace in more than 15 years.

Homes flipped in 2021 typically generated a gross profit of $65,000 nationwide (the difference between the median sales price and the median amount originally paid by investors). That was down 3 percent from $67,000 in 2020 and translated into just a 31 percent return on investment compared to the original acquisition price – the lowest margin since 2008. The latest ROI (before accounting for mortgage interest, property taxes, renovation expenses and other holding costs) was down from 41.9 percent in 2020 and 40 percent in 2019. The decline in the ROI also marked the steepest drop since at least 2005, resulting in margins that were commonly down by 20 percentage points from the 51 percent peak over the past decade, hit in 2016.

U.S. Home Flipping Gross Profits & Returns Chart

“While gross profits were lower for fix-and-flip investors in 2021, there may have been offsets that protected net profits,” said Rick Sharga, ATTOM’s executive vice president of market intelligence. “Fewer flippers financed their purchases, so their cost of capital was lower. And it took less time to execute a flip, reducing holding costs, and suggesting that less extensive – and less expensive – repairs were needed to bring the properties to market. A lot of the mark-up on fix-and-flip properties historically has come from the value of those repairs, but so have a lot of the costs that reduce net profits.”

2021 Gross Flipping ROI by Price Range Chart

Investors saw their gross profit margins dip for the fourth time in five years as the median value of the homes they flipped rose more slowly than the median price they paid to purchase properties – 21.1 percent versus 31.3 percent. The decline in home-flipping profits may represent a rare crack in the foundation of the U.S. housing market, which otherwise boomed in 2021 both because of and in spite of the worldwide Coronavirus pandemic.

Throughout the two-year-old pandemic, a surge of buyers has flooded the market amid a confluence of key factors. Tops among them have been a combination of historically low mortgage rates and a desire of many households largely unscathed financially by the pandemic to trade densely populated virus-prone areas for the perceived safety and wider spaces offered by a single-family home and yard.

Home flipping rates down in slightly more than half of local markets; biggest drops in Northeast and West

Home flips as a portion of all home sales decreased from 2020 to 2021 in 110 of the 209 metropolitan statistical areas analyzed in the report (53 percent). Nine of the 10 biggest decreases in annual flipping rates among MSAs came in the Northeast and West, led by Honolulu, HI (rate down 83 percent); Atlantic City, NJ (down 73 percent); Manchester, NH (down 57.7 percent); Rochester, NY (down 48 percent) and Cedar Rapids, IA (down 47.8 percent). Metro areas qualified for the report if they had a population of at least 200,000 and at least 100 home flips in 2021.

Aside from Rochester, the biggest decreases in flipping rates in 2021 across MSAs with a population of 1 million or more were in Las Vegas, NV (rate down 37.2 percent); Minneapolis, MN (down 36.7 percent); Sacramento, CA (down 36.3 percent) and Philadelphia, PA (down 35.4 percent).

Home flipping rates increased from 2020 to 2021 in 99 metro areas with sufficient data to analyze (47 percent). The largest annual increases in 2021 in the home flipping rate came in Provo, UT (rate up 114.3 percent); Salt Lake City, UT (up 113.4 percent); Austin, TX (up 111.2 percent); College Station, TX (up 97.4 percent) and Ogden, UT (up 95 percent).

Aside from Salt Lake City and Austin, the biggest annual flipping-rate increases in MSAs with a population of 1 million or more were in San Antonio, TX (rate up 56.2 percent); Dallas, TX (up 34.4 percent) and Houston, TX (up 32.3 percent).

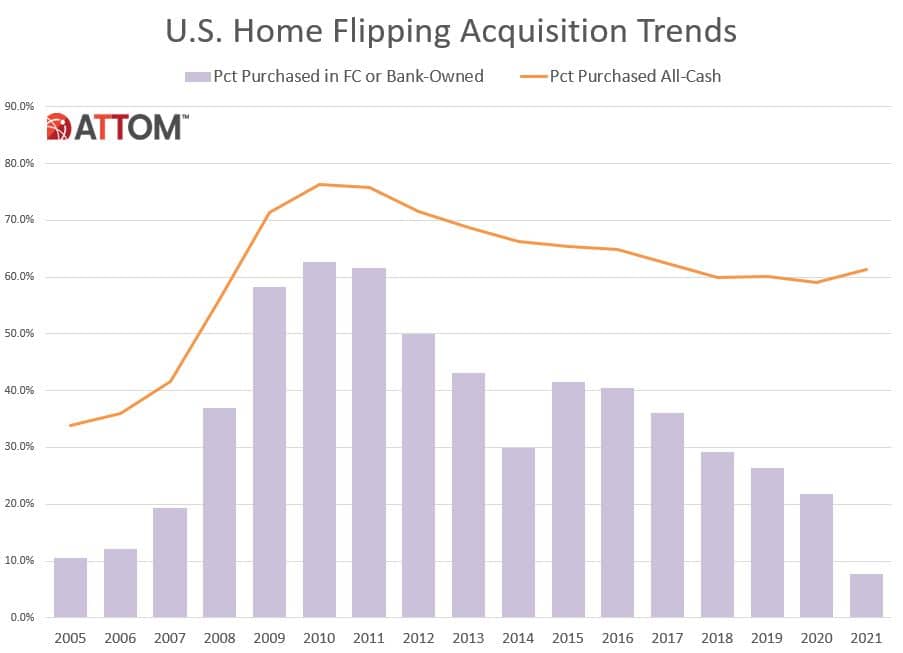

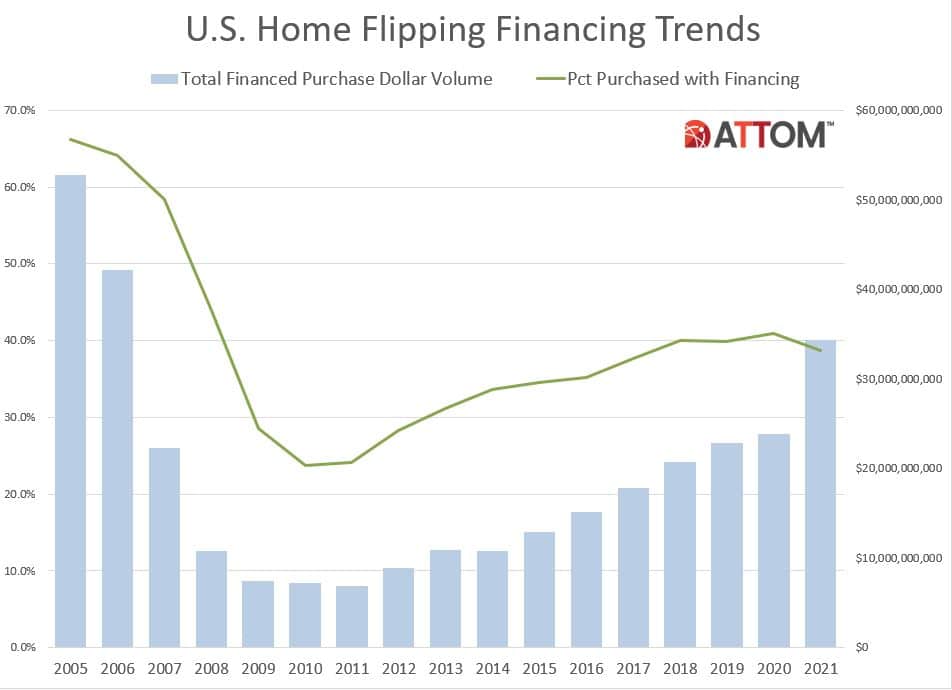

Share of home flips purchased with financing decreases to lowest level in three years

Nationally, the percentage of flipped homes purchased with financing decreased in 2021 to 38.7 percent, down from 41 percent in 2020 and from 39.9 percent in 2019. Meanwhile, 61.3 percent of homes flipped in 2021 were bought with all-cash, up from 59 percent in 2020 and from 60.1 percent two years earlier.

U.S. Home Flipping Acquisition Trends Chart

“In an environment where mortgage rates are rising as rapidly as they are today, investors buying with cash are at a distinct advantage over consumer homebuyers,” Sharga noted. “The combination of rising home prices, rising mortgage rates and rising inflation is undoubtedly creating affordability issues for many prospective buyers, so it’s possible that there will be less competition overall for the limited inventory of homes available for sale.”

U.S. Home Flipping Financing Trends Chart

Among metropolitan statistical areas with a population of 1 million or more and sufficient data to analyze, those with the highest percentage of flipped homes purchased by investors with financing in 2021 included Louisville, KY (55.6 percent); San Diego, CA (55.4 percent); Seattle, WA (52.6 percent); Portland, OR (48.6 percent) and San Francisco, CA (47.6 percent).

In that same group, the metro areas with a population of 200,000 or more that had the highest percentage of flips purchased with all cash included Tuscaloosa, AL (90.6 percent); Buffalo, NY (84.1 percent); Dayton, OH (82.8 percent); Detroit, MI (82.2 percent) and Canton, OH (82.1 percent).

Typical gross profits on home flips decline in 2021 after hitting 15-year high

Homes flipped in 2021 were sold for a median price nationwide of $275,000, with a gross flipping profit of $65,000 above the median original purchase price paid by investors of $210,000. That national gross-profit figure was down from a 15-year high of $67,000 in 2020 but still up from $60,000 in 2019.

Among the 53 metro areas in the U.S. with a population of 1 million or more, those with the largest gross-flipping profits in 2021 were San Jose, CA ($265,500); San Francisco, CA ($172,000); Seattle, WA ($149,950); San Diego, CA ($145,500) and Washington, DC ($139,555).

The lowest gross-flipping profits among metro areas with a population of at least 1 million in 2021 were in Kansas City, MO ($23,456); Houston, TX ($32,300); San Antonio, TX ($34,357); Dallas, TX ($40,800) and Atlanta, GA ($43,900).

Home flipping returns drop to 13-year low

With median resale prices on home flips rising more slowly in 2021 than they were when investors were buying properties, the gross profit margin on the typical flip in the U.S. last year fell to 31 percent – the lowest level since 2008. The 10.9 percentage-point drop from 2020 exceeded any decline since at least 2005.

Investment returns on median-priced home flips decreased from 2020 to 2021 in 186, or 89 percent, of the 209 metro areas analyzed.

Among metro areas with a population of 1 million or more, the biggest percentage-point decreases in profit margins in 2021 were in Cleveland, OH (ROI down from 101.5 percent in 2020 to 40 percent in 2021); Cincinnati, OH (down from 83.5 percent to 40 percent); St. Louis, MO (down from 71 percent to 39 percent); Columbus, OH (down from 70 percent to 40 percent) and Providence, RI (down 65.7 percent to 36.4 percent).

In that same group of markets with populations of at least 1 million, the only increases in returns on investment on the typical sales were in Buffalo, NY (ROI up from 92 percent in 2020 to 98.9 percent in 2021); Raleigh, NC (up from 14.5 percent to 19.8 percent); Nashville, TN (up from 33.3 percent to 36.8 percent); Boston, MA (up from 29.1 percent to 31.3 percent) and Phoenix, AZ (up from 20.8 percent to 21.3 percent).

Among metro areas with a population of at least 1 million, the biggest profit margins in 2021 were in Pittsburgh, PA (100.6 percent); Buffalo, NY (98.9 percent); Philadelphia, PA (92.3 percent); Baltimore, MD (81.3 percent) and Virginia Beach, VA (76.6 percent). The smallest were in Kansas City, MO (12.3 percent); Salt Lake City, UT (13.9 percent); Houston, TX (14 percent); Dallas, TX (16.1 percent) and San Antonio, TX (17 percent).

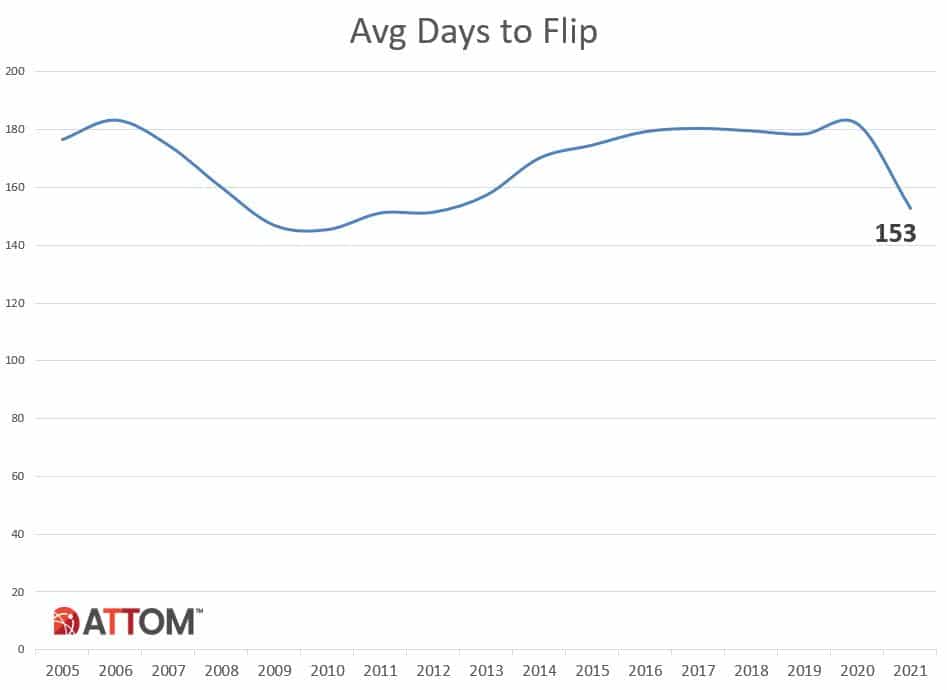

Average time to flip nationwide down to nine-year low

Home flippers who sold homes in 2021 took an average of 153 days to complete the flips, the lowest number since 2012. Last year’s average was down from 182 days for homes flipped in 2020 and 178 days in 2019.

Average Days to Flip By Year Chart

Percent of flipped homes sold to FHA buyers drops below 10 percent

Of the 323,465 U.S. homes flipped in 2021, just 8.2 percent were sold to buyers using a loan backed by the Federal Housing Administration (FHA). That marked the smallest percentage since 2007, and was down from 13.9 percent in 2020 and 14 percent in 2019.

Among the 209 metro areas with a population of at least 200,000 and at least 100 home flips in 2021, those with the highest percentage of flipped homes sold in 2021 to FHA buyers — typically first-time homebuyers — were Laredo, TX (26.5 percent); Yuma, AZ (22.5 percent); Visalia, CA (20.5 percent); New Haven, CT (19.9 percent) and Springfield, MA (18.9 percent).

Just 25 counties had a home flipping rate of at least 10 percent in 2021

Among 900 counties with at least 50 home flips in 2021, there were only 25 counties where home flips accounted for at least 10 percent of all home sales last year. The top five were McCurtain County, OK (northeast of Dallas, TX) (15 percent); Logan County, KY (north of Nashville, TN) (13 percent); Gilmer County, GA (north of Marietta) (12.4 percent); Fentress County, TN (northwest of Knoxville) (12.1 percent) and Greene County, GA (south of Athens) (11.7 percent).

Thirteen zip codes had a home flipping rate of at least 20 percent

Among 8,020 U.S. zip codes with a population of 5,000 or more and at least 10 home flips in 2021, there were 13 zip codes where flips accounted for at least 20 percent of all home sales, including six in Detroit, MI. The group with a flipping rate of at least 20 percent was led by 78701 in Travis County (Austin), TX (31.4 percent); 44730 in Stark County (Canton), OH (27.8 percent); 78705 in Travis County (Austin), TX (27.3 percent); 48205 in Wayne County (Detroit), MI (25.3 percent) and 48227 in Wayne County (Detroit), MI (23.1 percent).

High-level takeaways from fourth-quarter 2021 data:

- There were 96,773 home flips in the fourth quarter of 2021 which represented a flipping rate of 6.8 percent.

- The share of homes flipped in the fourth quarter of 2021 that were purchased by investors with financing represented 37 percent of all homes flipped in the quarter, down from 39.1 percent in the previous quarter and from 42.6 percent in the fourth quarter of 2020. The share purchased with cash rose to 63 percent, from 60.9 percent in the third quarter of 2021 and 57.4 percent in the fourth quarter of 2020.

- The median gross-flipping profit on home flips in the fourth quarter of 2021 was $65,000, which represented a typical 28.3 percent return on investment (percentage of original purchase price). That was down from 31.1 percent in the previous quarter and from 43.6 percent in the same period of 2020.

- Home flips completed in the fourth quarter of 2021 took an average of 154 days, down from 176 days in the fourth quarter of 2020.

Report methodology

ATTOM analyzed sales deed data for this report. A single-family home or condo flip was any arms-length transaction that occurred in the quarter where a previous arms-length transaction on the same property had occurred within the last 12 months. The average gross flipping profit is the difference between the purchase price and the flipped price (not including rehab costs and other expenses incurred, which flipping veterans estimate typically run between 20 percent and 33 percent of a property’s after repair value). Gross flipping return on investment was calculated by dividing the gross flipping profit by the first sale (purchase) price.

https://www.attomdata.com/news/home-flipping/attom-year-end-2021-u-s-home-flipping-report/

On the other hand, turnkey homes are ready to move in and these are what the vast number of homebuyers are looking for. They are also looking for the convenience of moving in over the weekend, putting the dishes in the cupboards, and going to work on Monday with minimal disruption to their lives. Compared to a rehab, homebuyers pay dearly for the convenience of a turnkey. That is why there is a strong market of investors that do the rehab in return for a substantial profit selling turnkey ready homes.

On the other hand, turnkey homes are ready to move in and these are what the vast number of homebuyers are looking for. They are also looking for the convenience of moving in over the weekend, putting the dishes in the cupboards, and going to work on Monday with minimal disruption to their lives. Compared to a rehab, homebuyers pay dearly for the convenience of a turnkey. That is why there is a strong market of investors that do the rehab in return for a substantial profit selling turnkey ready homes. From actually using their ovens to searching for available apartments by laptop instead of smartphones, renter behavior has clearly changed over the course of the pandemic, according to panelists at NMHC’s 2022 Apartment Strategies Conference in Orlando.

From actually using their ovens to searching for available apartments by laptop instead of smartphones, renter behavior has clearly changed over the course of the pandemic, according to panelists at NMHC’s 2022 Apartment Strategies Conference in Orlando.{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}