Investors snapped up $1.2 billion of bonds linked to a San Francisco office tower that makes up much ofDonald Trump’s fortune.

The AAA slice of the commercial mortgage-backed security sold Friday with a discount margin, or risk premium, of 125 basis points over one-month Libor -- roughly in line with other recent office-tower deals.

The bonds are being used to refinance a loan on the 555 California Street property in a deal that gives joint owners Vornado Realty Trust and Trump a $617 million payout.

The complex, among the tallest buildings in San Francisco, is one of two Trump-linked office towers that Vornado is refinancing. The other is in New York. While Vornado majority owns them, Trump’s 30% stake is the most valuable part of his portfolio, making up about one-third of his $2.3 billion fortune, according to the Bloomberg Billionaires Index.

The refinancing -- and cash windfall for Vornado and Trump -- comes months after several banks tied to the former president said they would no longer work with him after the deadly U.S. Capitol riot in January.

While the bond found strong demand, at least one investor was put off by the Trump connection.

“We looked at the deal and it did not pass our Environmental, Social, and Corporate Governance (ESG) process because of Trump’s poor record (going back to the 1990s) of not only paying back investors, but being difficult when he runs into difficulties,” John Kerschner, head of securitized products at Janus Henderson, said in an interview.

Kerschner said the offering priced tighter than some other “esoteric” office-tower CMBS deals with somewhat lower-quality properties, such as a recent deal underpinned by a loan on office towers in downtown Houston. On the other hand, the deal priced the same or slightly wider than some deals tied to higher-quality trophy towers, he added.

Proceeds of the 555 California Street CMBS will fund improvements to the buildings and return about $617 million to the owners, according to a marketing document obtained by Bloomberg.

“For a complex that couldn’t be sold last year, a large equity return is arguably the next best thing for the sponsor,” said Christopher Sullivan, chief investment officer at the United Nations Federal Credit Union. “It is a trophy property in a prime location with stable, high-quality diverse tenants and high occupancy for the area given the pandemic.”

Sullivan sees risks, though. The loan is structured as interest-only throughout, which may increase refinancing risk, on top of moderate leverage. Moreover, one-third of tenants also have the option to terminate their leases, “which is not surprising given the level of leasing or space-requirement uncertainties. However, it may present net cash flow risk,” he noted.

New York Next

Meanwhile, the refinancing of the New York tower at 1290 Avenue of the Americas is “on deck,“ Steve Roth, Vornado’s chief executive officer, said in a letter to shareholders earlier this month.

The refinancing comes after Vornado tried selling the two assets last year. It shelved the effort after not reaching its pricing goals.

“We found investors to be uncertain, distracted and handicapped by inability to travel,” Roth said in the letter to shareholders. “As markets improve, we may well revisit other alternatives for these two buildings,” he added.

Earlier this week, Eric Trump, executive vice president of the Trump Organization and Donald Trump’s son, described the properties as “arguably two of the best commercial assets anywhere in the country.”

Trump has at least $590 million in debt coming due in the next four years on other properties owned by the Trump Organization, more than half of which is personally guaranteed. Some of those properties, such as the company’s Washington, D.C., hotel and its golf resort near Miami, have suffered from plunging revenue during the pandemic.

“We are one of the most under-leveraged real estate companies in the country relative to our assets,” Eric Trump said.

On Wednesday, Fed chair Jerome Powell raised some eyebrows - and launched some sell programs - when in the middle of a lengthy tirade about how there is no inflation, soaring prices notwithstanding, he admitted that some assets were "frothy", yet paradoxically without acknowledging the Fed's explicit (and dedicated) role in creating and nurturing said market froth. Or, as Rabo's Michael Every put it, "the most surprising thing was Powell daring to use the word “froth” to describe the stock market he himself is boiling."

Fast forward just two days later, when moments ago Dallas Fed's non-voting president (and former Goldman partner), Robert Kaplan, doubled down on the "bad Fed cop" angle and says "we’re now observing excesses and imbalances in markets."

Explaining that he is "very attentive to that and that’s why I do think at the earliest opportunity, I think will be appropriate for us to start talking about adjusting those purchases”, Kaplan said that "we’ve got real excesses in the housing market” which is why he had not changed his view that rates should start to rise in 2022, and that the Fed should start talking about tapering of bond buying soon; most ominously - and an indication of just how much confusion there is at the Fed right now - he said that he expects to see a surge in prices of more than 2.5-2.75% in the coming months.

According to Kaplan, getting less-educated workers back to the workforce and in jobs is a challenge during the recovery. The former Goldman employee also reiterated the upside risk to his 6.5% growth forecast for the US economy and said that while “it’s not yet the speculative situation that we had back in ‘07, ‘08 and ‘09", he said that "it bears watching and keeping a close eye on."

His hawkish comments, which came alongside a report that a UK study has determined that individuals who have had only the first does of the Pfizer COVID-19 vaccine remain at risk against dominant new variants (except in those who have already had COVID-19) spooked markets and promptly put a damper on a modest rally that tried to emerge shortly after the US open.

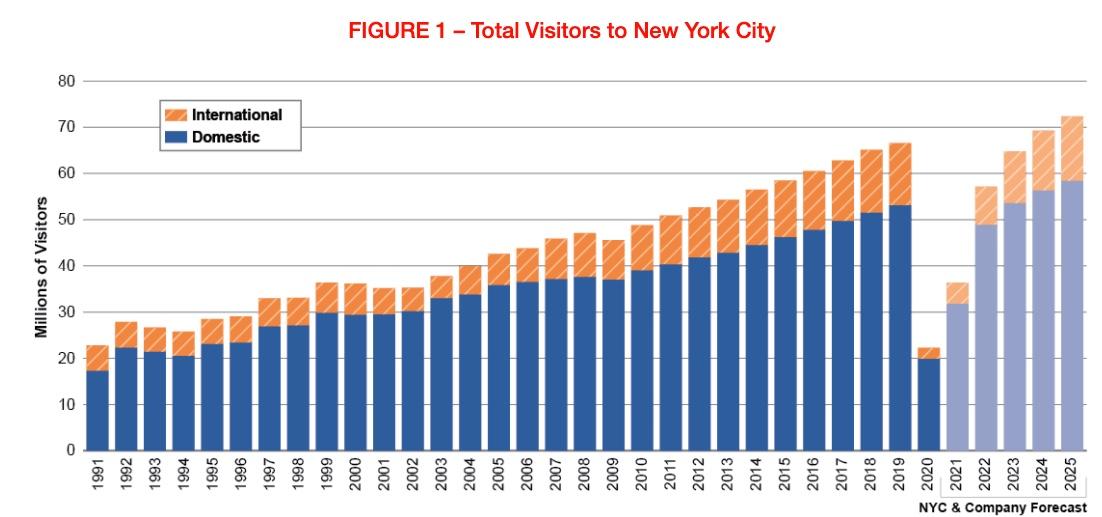

As Europe rolls out a vaccine passport to try and support its tourism industry by any means necessary, New York City's tourism industry is just showing its first signs of revival.

And with those who choose not to get vaccinated restricted from traveling abroad for the foreseeable future, domestic destinations like the Big Apple are excited by the prospect of a bigger-than-expected rebound. On that note, Bloomberg reports that the city's tourism industry is just showing its first signs of revival, according to a report from the state Comptroller's Office.pandemic.

Spending by visitors to New York City dropped by 73% in 2020 from the year before, costing the city $1.2 billion in lost tax revenue, as 43.7MM fewer visitors arrived in the city in 2020. This accounted for 59% of the $2 billion in lost revenue the city believes was lost due to the pandemic. What's more, the industry’s overall economic impact fell to $20.2 billion in 2020 from $80.3 billion in 2019.

Prior to the pandemic (September 2019), hotel occupancy in the City was 89.6 percent, the highest in the nation, and was a key factor attracting hotel builders and operators. By September 2020, occupancy had dropped to 38.9 percent, pressuring daily room rates.

While the first green shoots are starting to show, New York Comptroller Thomas DiNapoli said it will take years for the industry to fully recover.

"The pandemic’s damage to this industry has been staggering and it may take years before tourism returns to pre-pandemic levels," Comptroller Thomas DiNapoli said in a statement on Wednesday. "Visitors and their spending are essential factors in measuring the health of the economy."

Over the past few decades, NYC's services-based economy has become increasingly dependent on tourism, as any panhandler in Times Square would likely attest.

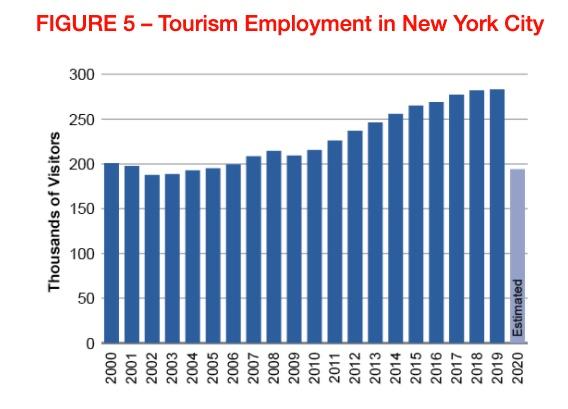

Tourism jobs declined by more than 30% last year, from 283K to 194K, a loss of 89K jobs, numbers that - according to the latest nonfarm payrolls data, are finally creeping higher.

Since 1991, the number of visitors to the City has nearly tripled, with almost half the growth occurring in the last 10 years (between 2009 and 2019). Much of this has been driven by international tourism, although with the US's lingering travel restrictions, international travelers have seen by far the biggest drop. Though, to be sure, the majority of visitors to the city are still domestic travelers. But generally speaking, the city makes more money off of international tourists, with one international tourist typically spending 4x what a domestic tourist spends. Unsurprisingly, the majority of these jobs are located in Manhattan, though Brooklyn and Queens have seen rapid tourism job creation over the last 10 years.

Tourism industry employees, like hospitality workers, tend to live in the city. According to the report, 83% of the nearly 200K workers live in the city. A higher share are also self-employed. There are 60,800 firms in New York City that provide at least some of their services in support of tourism. Of these, 39.5 percent are located in Manhattan, while Brooklyn and Queens also account for large portions (25.3 percent and 22.5 percent, respectively).

Of course, even as international travelers start to trickle back once COVID-19 case numbers have returned to zero, it's looking increasingly possible that a new scourge might take its place: violent crime, which is exploding in the city in the wake of the pandemic.

Urban single-family prices have jumped nearly 20% year-over-year to $286,000, which is faster than any other type of home and the biggest increase of record for those homes, according to a new report from Redfin.

In another sign that people are returning to the city, condos sales are up 30% year over year, which is more than any other home type.

Still, regardless of neighborhood, single-family homes are selling faster than condos. For instance, suburban single-family homes spent 25 days on the market before going under contract during the 12 weeks ending April 4. Urban single-family homes are spending a median of 29 days on the market before going under contract.

While the popularity of urban single-family homes indicates that people still prize space and self-contained homes without shared walls, urban condos sales were up nearly 30% year over year during the 12 weeks ending April 4. That represents a bigger increase than any other home category and provides notice that the condo market is clearly in recovery after plummeting last summer. Coming in second were suburban condos, which saw sales rise 22.8% year over year.

“Many homebuyers are still prioritizing features that were desirable at the beginning of the pandemic, like space for a home office or a big backyard, partly because many people plan to continue working from home,” said Redfin economist Taylor Marr in a prepared statement. “But as people venture out of their homes more often, they’re rediscovering the advantages of living in a city.”

Before people buy, they’re searching for homes. Online listings of homes in large cities experienced a 62% year-over-year increase in page views, which was bigger than the 30% gain for small towns and the 18% increase for rural areas. Redfin does note that the large year-over-year jump in pageviews for large metros is likely exaggerated because March marks one year since the pandemic hit the US.

“The fact that homebuyer interest in large metros is accelerating while it’s decelerating in rural areas and small towns suggests the pandemic-driven bump in demand for rural properties has peaked and buyers are returning to the city,” according to Redfin.

While the home sales market is so hot that some people are comparing the frenzy to the mid-2000s, more inventory could be on the way to ease some of the pressure.

A recent study from realtor.com and HarrisX found that help is on the way for both trade-up and first-time buyers. Ten percent of homeowners in the US plan to sell within the next 12 months, which is 25% more than the share of homes that come to market in a typical year, according to realtor.com. In addition, 16% of homeowners are likely to list their homes in the next two to three years.

The city announced Tuesday it will soon deploy 80 cops to Midtown to combat vagrancy and safety issues.James Keivom Hell’s Kitchen residents fear a summer of the “living dead” as thousands of vagrants the city dumped in the neighborhood over the last year emerge from their homeless hotels.

A “sewer” and a “cesspool” is how longtime Hell’s Kitchen activist Marisa Redanty described the neighborhood in recent weeks, as the return of warm weather produced a sudden upswing in the presence of drug-addled and deranged homeless people on the streets of Midtown.

“This summer will be the night of the living dead,” she predicted.

NYPD data shows the area’s homeless hotels have already become quality-of-life hellscapes.

Police, EMS and fire have responded to 233 calls already this year at Spring Hill Suites on West 36th Street, compared with just 22 calls at the same time last year when the city began moving shelter residents into hotels in April.

Skyline Hotel on 10th Avenue has become a hotspot for crime.James Keivom

At the Four Points Sheraton on West 40th, the number of 911 calls has grown from 54 to 198.

At the now notorious Skyline Hotel on 10th Avenue, police have already responded to 392 calls in 2021 — nearly four per day — compared with 72 at the same time last year.

State records show that two Level 3 sex offenders — the most dangerous classification — are living at the Skyline, including one former member of New York state’s 100 most wanted fugitives list, just steps from three city high schools on 50th Street.

In one Hell’s Kitchen incident, 24-year-old mom Alyssa Owens was charged with killing her own 2-month old baby at the Candlewood Suites Hotel on West 39th Street in January.

The Four Points by Sheraton is one of many locales that has seen a sharp rise in crime.Helayne Seidman

The neighborhood’s homeless crisis gained nationwide attention last month when Vilma Kari, 65, was savagely attacked in broad daylight on West 43rd Street in an assault caught on viral video.

The alleged attacker, Brandon Elliott, 38, is a convicted killer who murdered his own mother in 2002 and had been living at the Four Points Sheraton on West 40th, raising concerns that other violent ex-cons are freely walking the streets of Hell’s Kitchen.

Alyssa Owens killed her baby at Candlewood Suites Hotel in January.Robert Miller

Neighbors cite a visibly ugly increase in trouble spilling out of the hotels and onto the sidewalks: theft, drug abuse, public defecation, open-air sex and random violence.

“It’s dangerous, very dangerous,” said Dan DePhamphilis, who manages Rudy’s Bar and has lived in the neighborhood for more than 30 years. The cameras outside his Ninth Avenue watering hole have captured everything from drug deals to gunfire over the past year, he said.

“Our leaders have destroyed the city and Hell’s Kitchen has been a focal point.”

Surveillance video recorded a couple smoking what appeared to be crack and having sex outside Rudy’s below-grade doorway, the daylight from Ninth Avenue shining down on them just steps away. The stairway entrance has since been boarded over.

The area has become rife with drug use.

Two weeks ago, across the street from Rudy’s, a belligerent customer at Five Napkin Burger at the corner of 45th Street punched the restaurant’s manager.

Mayor de Blasio rushed to move homeless-shelter residents into hotel rooms in the early days of the COVID outbreak, believing such spaces would be safer than congregate shelters. Hell’s Kitchen landed a hugely disproportionate number of those homeless residents.

Business managers like Danny DePamphilis are concerned for the neighborhood.James Keivom

The city turned 67 hotels across all five boroughs into shelters, according to the Department of Social Services – 10 of those landed in Hell’s Kitchen.

Manhattan Borough President Gale Brewer noted in a September 2020 letter to Department of Social Services Commissioner Steven Banks obtained by The Post that more than 2,100 homeless were relocated to Manhattan Community District 4, which includes both Chelsea and Hell’s Kitchen.

“The density of the transfer,” wrote Brewer, “has strained the ability of the community to absorb it.”

Hizzoner pledged to move the city’s homeless out of hotels and back to shelters – but offered no timeframe.

People gather outside the Radisson Hotel on 525 8th Ave.James Keivom

“We absolutely are planning to, first of all, ensure that folks who have been in hotels go back into shelter settings, because shelter settings are where people can get the proper mental health support,” de Blasio said during an April 6 press conference.

The Department of Homeless Services “is keeping [the timeline] very close to the vest,” Brewer told The Post.

The city announced Tuesday it will soon deploy 80 cops to Midtown to combat vagrancy and safety issues — but that has done little to assuage neighborhood concerns.

“Overnight the streets were loaded with sh-t. People sh-tting in the streets,” said Steve Olsen, the owner of West Bank Cafe on West 42nd Street

Danny DePamphilis manages Rudy’s Bar.James Keivom

“The cops can’t hurt. But they are in a helpless, thankless position, especially with catch-and-release laws.”

In addition to the 10 homeless hotels are six local, long-standing facilities dedicated to homeless and addiction services, according to a map provided by the Garment District Alliance, in conjunction the Hell’s Kitchen Neighborhood Alliance and Community Boards 4 and 5.

Most of these 16 facilities are clustered around the Port Authority Bus Terminal, offering a hellish, high-capacity gateway for criminals from other neighborhoods.

“Many of the problems are not necessarily caused by the residents of those hotels, but from friends, associates, and others such as drug dealers, pimps and others who prey upon those residents,” said Jerry Scupp of the Garment District Alliance.

Redanty said some local eateries have become hubs for outside gangs and dealers to sell drugs to the neighborhood’s large population of willing customers.

Marisa Redanty currently describes the area as a sewer” and a “cesspool.”James Keivom

The Midtown South precinct, which includes the bus terminal, reports robberies, felony assaults and burglaries more than doubled in the the first quarter of 2021 from the same period last year, even though far fewer people are out now compared to the first three pre-pandemic months of 2020.

DePhamphilis of Rudy’s Bar said “every small business” on Ninth Avenue has been robbed over the past year.

“All day long I watch it out the windows,” said Paul Fable, whose family has operated Poseidon Bakery on Ninth Avenue for 98 years. “The drug deals, people walking by stealing food off the tables at the restaurant across the street. DHS needs more protocols on what’s allowed. There’s gotta be some consequences. There’s gotta be some law and order.”

Fable now protects his business with a baseball bat.

The crime has led Poseidon Greek Bakery owner Paul Fable to take drastic measures.James Keivom

Politics has made it nearly impossible for police to enforce that law and order, said NYPD officer Ed Mullins, president of the Sergeants Benevolent Association.

“There is a direct correlation between public policy and rising crime,” said Mullins, citing among other issues legislation passed just last month making New York City the first municipality in America to end qualified immunity for police officers, while catch-and-release bail reform mean criminals are swiftly back out on the streets.

“De Blasio has been the worst mayor in New York City as long as I can remember,” said Mullins, “coupled with a City Council that passes legislation they know is wrong.”

Another persistent problem is that the partnership of public money and private non-profits used to run the city’s homeless shelters is riddled with corruption, as The Post reported last month. Victor Rivera, founder of the Bronx Parent Housing Network, was recently charged by the Feds in a bribery and kickback scheme. Hotel-shelter operator Childrens Community Services was charged last year with bilking millions from taxpayers.

Hell’s Kitchen resident Sal Salomon has spent time in both prison and the city’s homeless shelter system, including its hotels, before finding his own place in recent months. He said hotels are ill-equipped to cope with homelessness issues, ranging from food to safety to access to mental healthcare.

“Everything that goes on in prison goes on in the shelters, but they keep it out of the media,” he said. “The fighting. The drugs. The shelters are worse than prison. At least in prison you know you’re in prison. Even the food in prison is better.”

Sal Salomon has previously said he “agrees” with the concerns surrounding homeless people living in hotels.J.C. Rice

Residents of the city’s hotel shelters are fed microwaved box meals, Salomon said. “In prison they cook for you.”

Matt Fox, the owner of Fine and Dandy, a boutique on West 49th Street near the Skyline Hotel, said the worst is yet to come for local businesses if the city doesn’t solve the Hell’s Kitchen homeless crisis soon.

“We need our tourists back and to get them we need our hotels back. The city has taken too long to sort out the problem,” said Fox. “There’s a narrative that small businesses that have made it this far have made it. But we might see more businesses close in the next couple months than we have in the past year if something doesn’t change soon.”

NYPD officer Ed Mullins, president of the Sergeants Benevolent Association called Mayor de Blasio “the worst mayor in New York City as long as I can remember.”James Keivom

Asked Fable of Poseidon Bakery: “How long does this go on? How long does our neighborhood have to suffer?”

Amazon-backed home technology solutions provider SmartRent.com Inc said on Thursday it had agreed to go public through a merger with a blank-check firm backed by venture capital firm Fifth Wall, valuing the equity of the combined company at around $2.2 billion.

The deal with Fifth Wall Acquisition Corp I is expected to provide the merged entity with $513 million in gross proceeds, comprising about $155 million from investors including Koch Real Estate Investments, Baron Capital Group, Lennar Corp and Invitation Homes.

SmartRent develops tech products for property owners and homebuilders that automate daily operational processes such as parking management, locks and thermostat operation. The Scottsdale, Arizona-based firm's customers include Lennar, Invitation Homes and Essex Property Trust Inc.

FWAA, a special purpose acquisition company (SPAC) raised $345 million through an initial public offering in February.

SPACs are publicly listed shell companies that raise funds to take a private company public through a merger at a later date, allowing the private firms to sidestep a traditional IPO to enter public markets.

J.P. Morgan Securities LLC and Morgan Stanley are acting as co-financial advisers to SmartRent while Deutsche Bank Securities and Goldman Sachs are acting as capital markets advisors to Fifth Wall Acquisition Corp I.

New York will no longer offer some state tax benefits to real estate investors funding Opportunity Zone projects, dealing another blow to the program and developers taking advantage of it.

A measure pushed by New York state Sen. Michael Gianaris to decouple New York state’s capital gains tax code from the federal program was included in the recently passed state budget. The change means developers and investors cannot defer state taxes on profits from asset sales poured into Opportunity Zone funds.

“Opportunity Zones are nothing more than a giveaway of public money to wealthy developers, and I’m glad New York took a stand against the much-abused program,” Gianaris said in a statement. The state’s action was previously reported by the New York Daily News.

New York joins North Carolina, California, Massachusetts and Mississippi in separating its state tax regime from the federal Opportunity Zones program.

The program, which was created by Republicans’ 2017 tax overhaul, lets investors and developers defer or forgo some capital gains taxes by funding projects in any of 8,700 Opportunity Zones across the country.

New York has 514 census tracts included in the program. Developers will still qualify for federal tax breaks for investing in those so-called distressed areas.

It’s unclear if there will be any immediate or major ramifications for Opportunity Zone projects in the state. Ken Weissenberg, a tax partner at EisnerAmper, said the elimination of the tax benefit makes New York more unfriendly to investors.

“[It’s] another wedge to drive people out of New York,” said Weissenberg.

But Daniel Ryan, a tax attorney at Sullivan & Worcester, believes that the impact of the state’s measure will be marginal. He said his clients are more interested in the federal tax benefit or whether a project makes financial sense.

“I don’t think state tax moves the needle,” said Ryan.

More than two dozen groups, including the New York State United Teachers and Communication Workers of America, recently wrote a memo supporting the elimination of the tax break. Those groups argued that the program could cost New York City and state up to $63 million in tax revenue during a “historic budget crisis.” (Legislators ultimately raised taxes $4.3 billion in passing a record-high $212 billion budget.)

The program purports to uplift low-income communities, but critics say the only thing it does for sure is save developers money. A small number of areas where development was already occurring — such as Hudson Yards on Manhattan’s Far West Side, or parts of Long Island City — make up the bulk of Opportunity Zones in the city.

President Joe Biden has said he intends to keep the Opportunity Zones program, but add transparency measures to see if it is actually helping low-income people.

175 Park Avenue, aka Project Commodore. Rendering by Skidmore Owings & Merrill

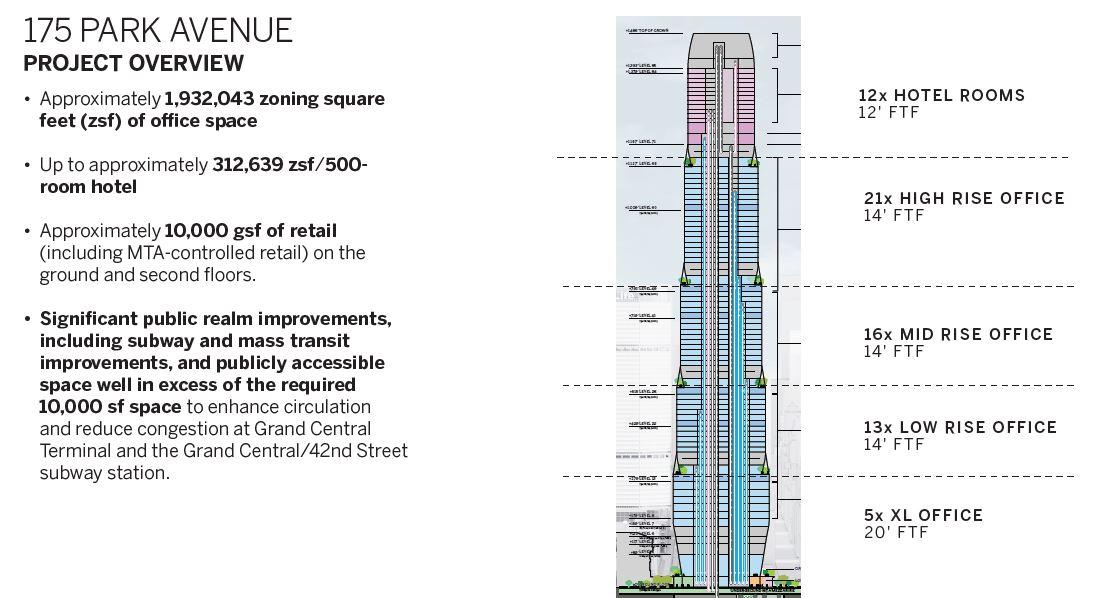

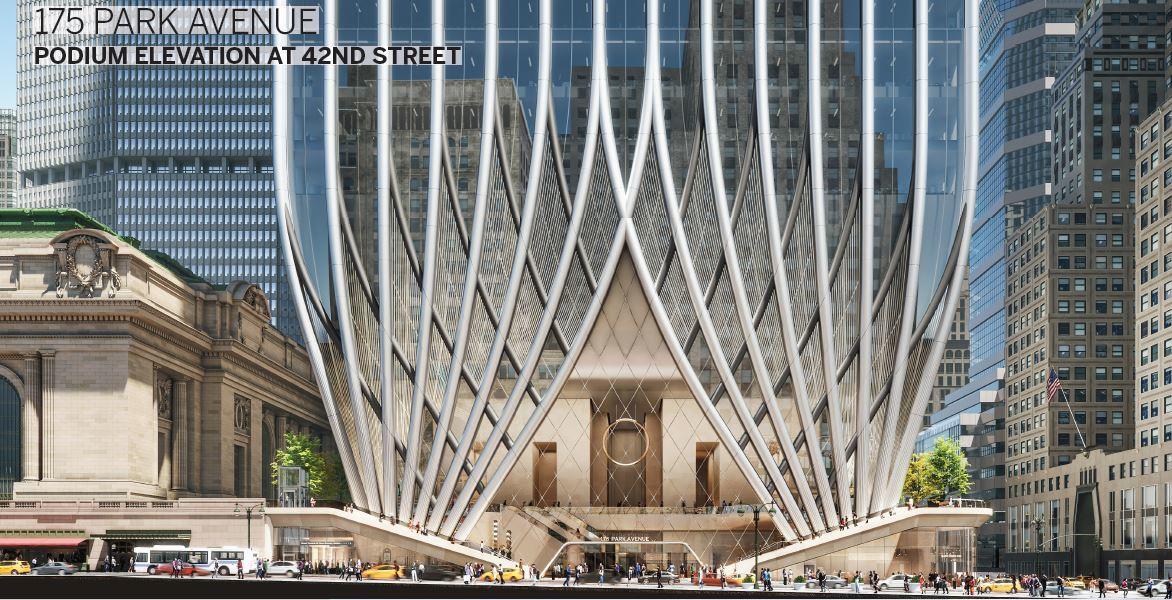

YIMBY spotted a new batch of renderings and diagrams that depict Project Commodore, Skidmore Owings & Merrill‘s upcoming mixed-use supertall at 175 Park Avenue in Midtown East. The 83-story behemoth is slated to rise at the corner of East 42nd Street and Lexington Avenue, on the site of the Grand Hyatt between the 108-year old Beaux Arts Grand Central Terminal and the 91-year-old Art Deco Chrysler Building. RXR Realty and TF Cornerstone are developing the massive structure, which also appears to have gotten a height reduction to 1,486 feet tall, as opposed to the 1,646-foot-tall architectural height previously announced. Inside will be 500 Hyatt hotel rooms on the upper floors spanning 453,000 square feet; 10,000 square feet of retail space on the ground, cellar, and second levels; new elevated, publicly accessible plaza space overlooking the surrounding Midtown neighborhood; and 2.1 million square feet of Class A office space.

Aerial renderings show Project Commodore making a dramatic presence over Midtown, despite a slight chop in the final height of the superstructure. Also added to the future skyline perspective is J.P. Morgan’s new supertall office headquarters at 270 Park Avenue, while Kohn Pedersen Fox’sOne Vanderbilt, the Chrysler Building, and Rafael Vinoly’s432 Park Avenue are also prominently seen in comparison with SOM’s future project. Each of the renderings and diagrams were from a slide presentation that Global Strategy Group presented to the Public Design Commission at last month’s public meeting as part of the conceptual review for Project Commodore, which received a large amount of positive reviews and feedback from the commissioners.

175 Park Avenue, aka Project Commodore, amongst the Midtown East skyline. Rendering by Skidmore Owings & Merrill

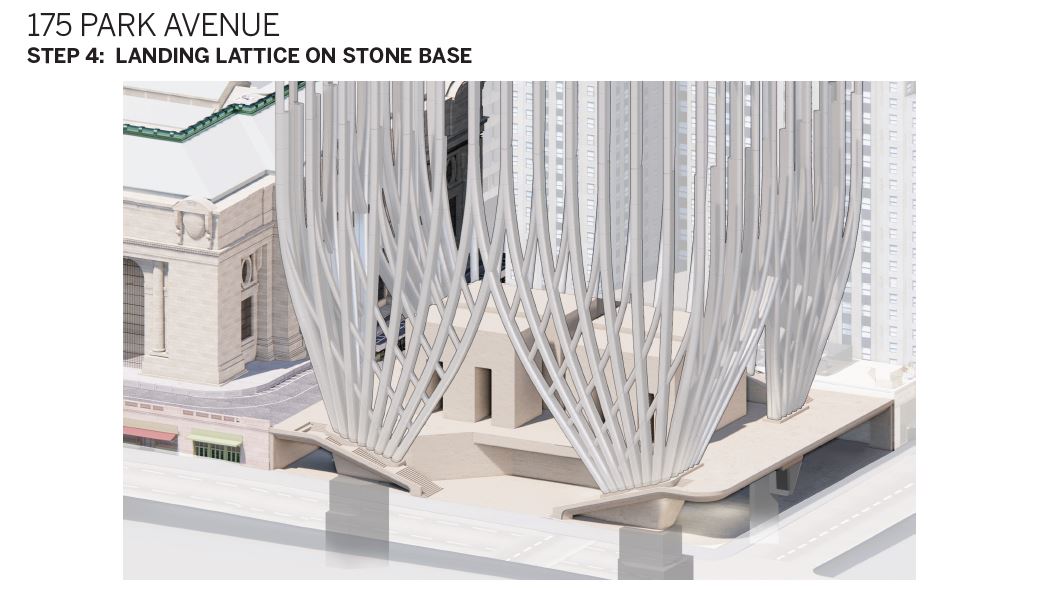

The intricate lattice crown would easily distinguish it from the rest of the nearby supertall rooftop parapets.

175 Park Avenue, aka Project Commodore. Rendering by Skidmore Owings & Merrill

Below is a diagram that outlines the buildings along 42nd Street between One Vanderbilt and the Chrysler Building and how the scale between each edifice is seen. This also gives a true sense of how Grand Central will be surrounded by two equally mammoth 21st century buildings.

175 Park Avenue, and the surrounding buildings along 42nd Street. Rendering by Skidmore Owings & Merrill

175 Park Avenue’s floor plates are substantially devoted to office space, while the hotel portion will be placed on the upper levels.

175 Park Avenue’s southern corner along 42nd Street and Lexington Avenue. Rendering by Skidmore Owings & Merrill

Steps leading to the terraces from 42nd Street. Rendering by Skidmore Owings & Merrill

An updated rendering showcasing the base of the southern elevation gives us more details on the symertical façade and its components.

175 Park Avenue’s southern base along 42nd Street. Rendering by Skidmore Owings & Merrill

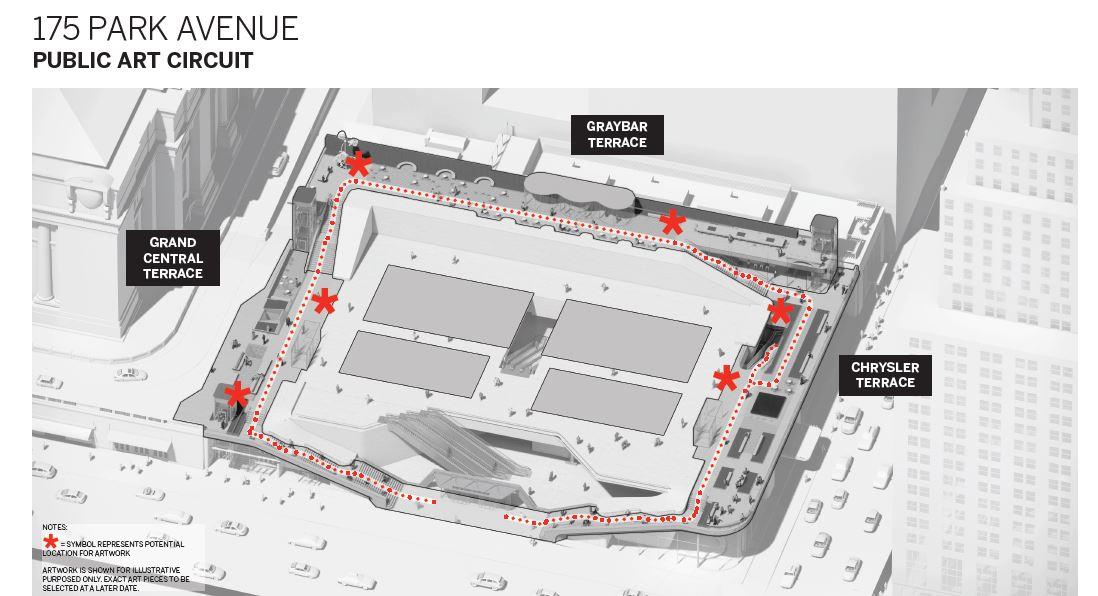

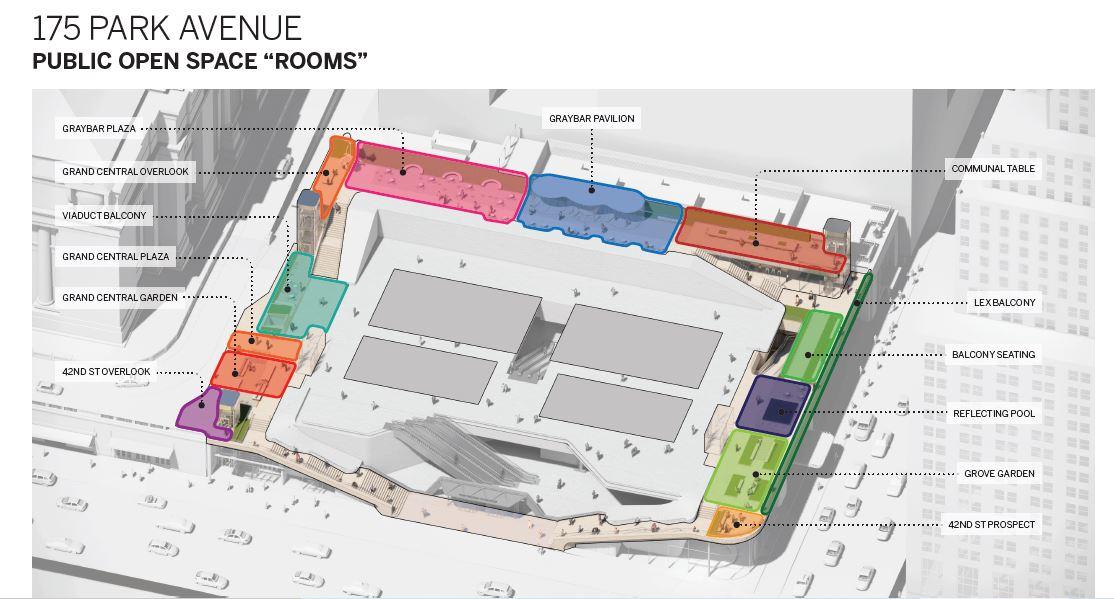

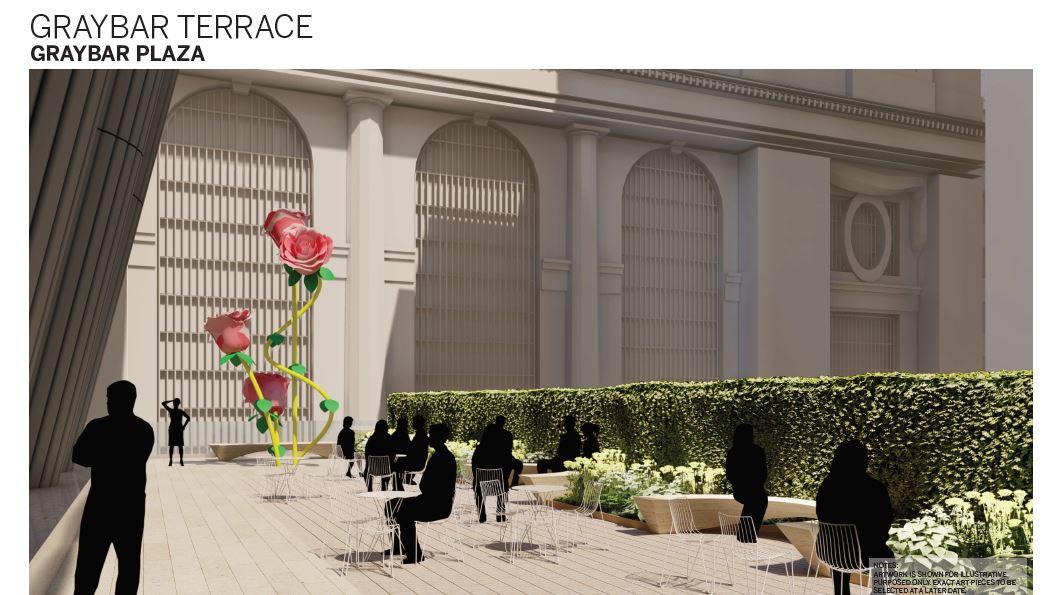

Steps would lead from the sidewalk to a wraparound elevated public terraces divided into three spaces: the Chrysler terrace, the Graybar terrace, and the Grand Central terrace. These three areas would then have a number of different aspects like reflecting pools, cafes, seating, landscaping and gardens, art sculptures, and overlooks.

Diagram by Skidmore Owings & Merrill

Diagram by Skidmore Owings & Merrill

Diagram by Skidmore Owings & Merrill

Diagram by Skidmore Owings & Merrill

Diagram by Skidmore Owings & Merrill

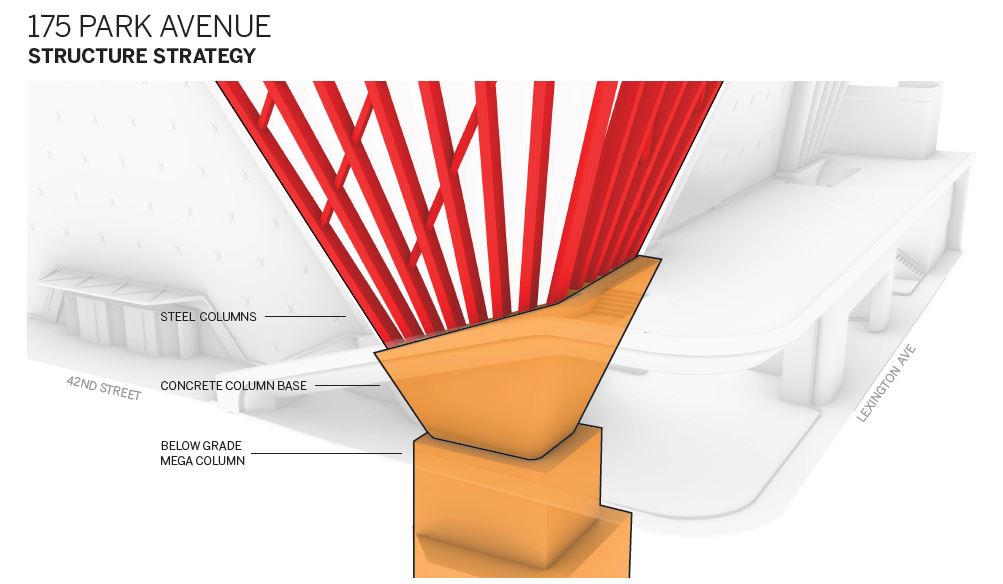

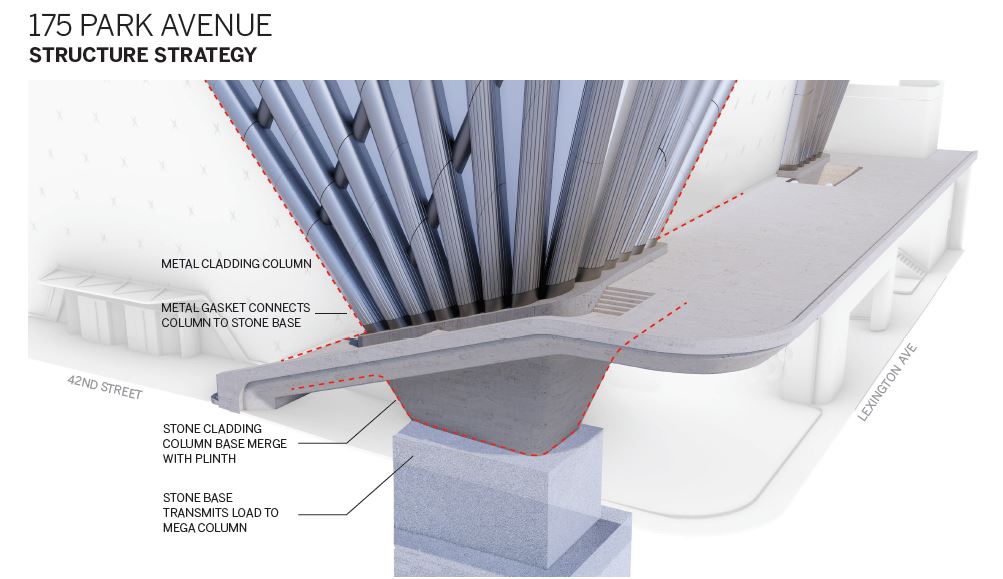

Other diagrams go into some more depth about the corners of 175 Park Avenue and how they will anchor the superstructure and connect it with the base.

Diagram by Skidmore Owings & Merrill

Diagram by Skidmore Owings & Merrill

Diagram by Skidmore Owings & Merrill

Diagram by Skidmore Owings & Merrill

Diagram by Skidmore Owings & Merrill

The next major step in the development is Uniform Land Use Review Process (ULURP), which is expected to occur at the end of 2021. An approval would then be followed by an 18-month-long demolition of the Grand Hyatt, and eventually proceed with the construction of 175 Park Avenue itself. Click here to read YIMBY’s previous updates about Project Commodore.