2022 has already had its fair share of bad news for mortgage rates, but this week was not to be outdone. It began as just another reasonably bad week with rates moving moderately higher, but still safely under the recent 13 year high seen on the morning of May 9th. But it ended with one of the worst days on record in more than a decade.

Sound a little dramatic? Sadly, it was. The average lender increased 30yr fixed rates by at least a quarter of a point (0.25%). That's only happened 4 other times since our daily record keeping began in 2009, and 3 of those were during the once-in-a-lifetime volatility that followed the onset of the pandemic. That made this the 4th worst week since 2009 as well.

When the smoke cleared, the average conforming 30yr fixed rate was as high as it's been since November 2008.

If that line looks a little steep recently, that's because with barely half of it in the books, 2022 has been the worst year for rates since 1979.

Whether we're talking about the short term drama on Friday or the bigger picture rout in 2022, the culprit is the same: inflation.

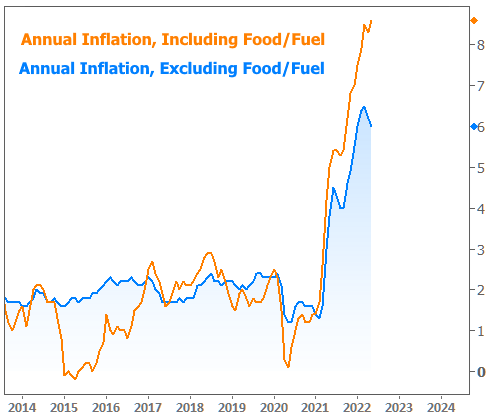

There are many ways to measure it, but if markets could only choose one inflation report to rule them all, it would be the monthly Consumer Price Index (CPI). The following chart shows overall CPI (including food/fuel) and "core" CPI which excludes food and fuel:

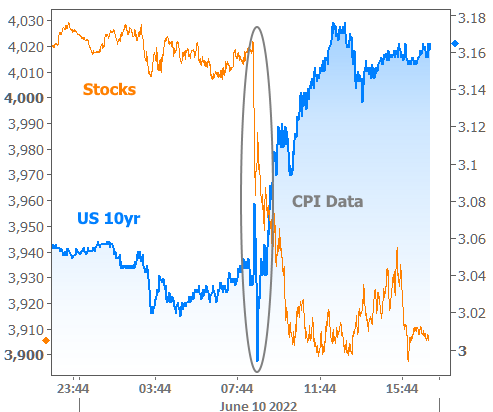

Both the headline and core CPI readings were higher than markets were expecting. Neither stocks nor bonds enjoyed the news.

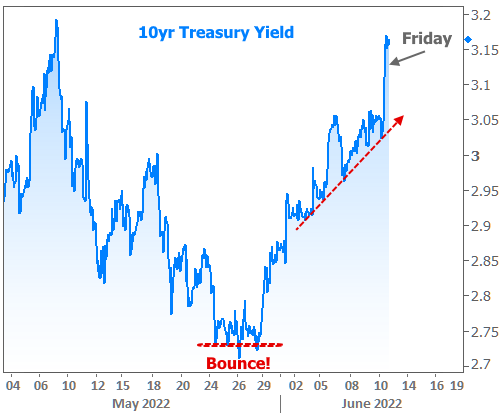

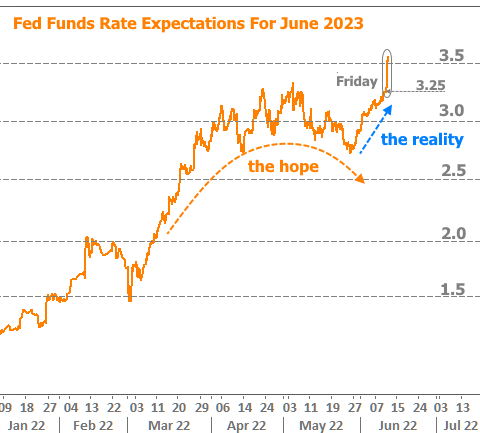

One of the reasons markets were so affected is the recent buzz about inflation showing signs that it might be leveling off. That buzz was responsible for rates having several solid weeks in May (inflation is a key driver of interest rates). But after European inflation set a record on May 31st, rates changed course abruptly. The trend was actually fairly linear over the past 2 weeks before Friday took things to the next level. (NOTE: the 10yr Treasury yield is a preferred benchmark for longer-term rates, in general).

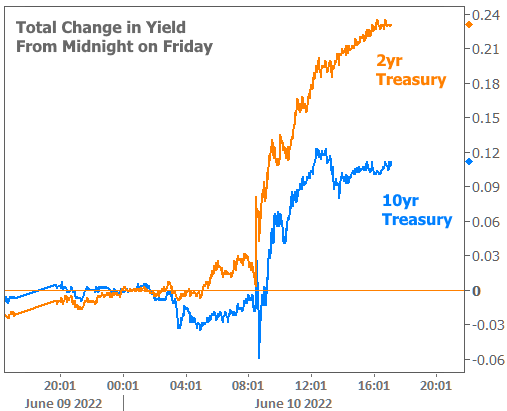

Other rates had it even worse than the 10yr.

Why would 2yr Treasuries take the news harder than the 10yr? It's simple enough: the most basic rate in all the land is the Fed Funds Rate set by the Federal Reserve. It applies to the shortest-term loans with time frames less than one day. Because a 2yr Treasury is much closer to the Fed Funds Rate than the 10yr Treasury, 2s feel it more when Fed Funds Rate expectations change. And change they did!

There are actually financial contracts that track the market's expectation for the Fed Funds Rate (Fed Funds Futures, to be exact). Like other rates, they began to level off in May as hopes swelled that inflation was falling into line. Like other rates, they began to move back up in June. But Friday saw some of the biggest single-day movement in Fed Funds Futures with an entire quarter of point change in a matter of hours.

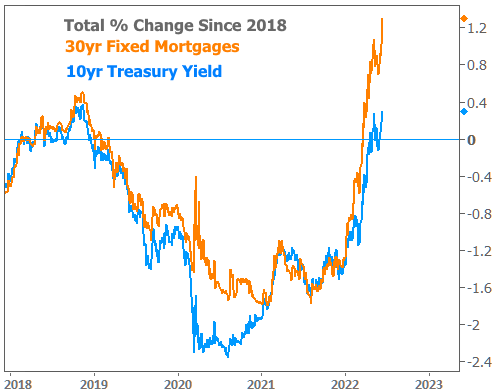

Incidentally, mortgages have inherently shorter average life spans than 10 years (even though 30yr mortgages may be common, people tend to sell or refi long before the 30 years are up). Life span expectations for mortgages are especially short right now because we expect to see rates move down enough to motivate refinance demand at some point in the next few years. As such, mortgage rates are behaving like bonds that are also closer to the Fed Funds Rate than 10yr Treasuries. Combine that with a generally less friendly stance from the Fed on its mortgage holdings and the underperformance of the mortgage market has been quite pronounced in 2022.

Even after all of the rationalization above there was still something a bit too abrupt about Friday. We need one more x-factor to help explain why things got so out of hand. That x-factor is easily found in next week's event calendar. The Fed will be out at 2pm ET on Wednesday afternoon with its latest policy announcement.

This doesn't mean the Fed is more likely to hike rates any higher than previously expected. Rather, markets are interested to see what the Fed has to say about the future path of rate hikes. Wednesday's meeting is in a strong position to comment on the forward outlook because it is one of the 4 meetings per year where the Fed also releases updates economic projections. These include the popular "dot plot" which the Fed uses to visually represent where each Fed member expects to see the Fed Funds Rate in the next few years.

While the Fed has repeatedly told the market not to read too much into "the dots," the market never listens. With CPI coming in hot this week, markets can't help but imagine some of those dots are going to drift higher than they otherwise would have. In that sense, Friday was merely the market's way of getting in position for Wednesday's potentially bad news. Mortgage rates were one of many casualties, but they did take extra damage because the Fed is considering selling some of its mortgage holdings at some point. While they have promised that's a ways off AND that they'd give ample warning, big surges in inflation could move that warning higher on the Fed's to-do list.

So is there any hope? Yes, in fact, there's quite a lot of hope! This month's CPI was rotten, but inflation is definitely taking a toll on the "demand" side of the economy now. Rates have also risen so quickly that there's a case to be made for a corrective momentum building up. All that would be necessary to release that momentum would be for inflation to actually find its footing. Perhaps it was just a month or two too soon for the data to confirm such things, but as soon as it happens, rate momentum will only have 2 options: sideways and lower.

https://www.mortgagenewsdaily.com/markets/mortgage-rates-06112022

No comments:

Post a Comment