In a stunning rebuke, echoing very closely our own concerns, Boston Fed President Eric Rosengren has – without naming-names – called out the WeWork business model as being a systemic risk to the US economy.

Two weeks ago we asked (rhetorically)…

zerohedge@zerohedge

Here is the problem as we laid it out:

While the collapse and/or bankruptcy of WeWork would hardly lead to a personal finance disaster – SoftBank’s Masayoshi Son is already Japan’s richest man and with a net worth of over $20 billion can easily stomach losing billions on WeWork (and Uber) – it would send shockwaves across US commercial real estate, as the company is already the single biggest tenant in New York City, as well as Chicago, Denver and central London.In fact, with over $47 billion in lease liabilities, WeWork is already one of the world’s largest lessees, trailing only oil exploration giants Petrobras and Sinpec, an astonishing feat for the flexible office space provider “which was founded less than a decade ago, bleeds cash, and doesn’t plan to become profitable any time soon.”As Bloomberg recently noted, “anyone weighing whether to buy shares in WeWork’s IPO cannot ignore the fact that the company will have to find $47 billion from somewhere in coming years to meet its contractual obligations – including about $10 billion in just the next five years. Right now, its own very negative cash flows won’t cut it.”

And now, it appears, Eric Rosengren has realized just how serious this leveraged debacle has become. In a speech delivered to New York University today – following his already hawkish tone from this morning by which he highlighted The Fed’s easy money policy has enabled record leverage – the Boston Fed head seems to have seen the light, fearing financial instability from WeWork and its ilk…

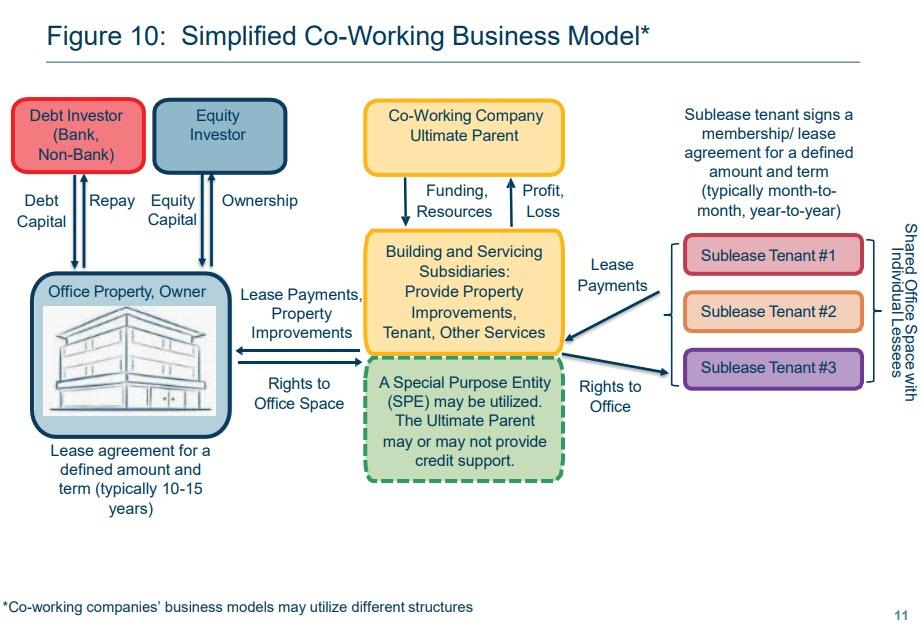

Mr. Rosengren noted the risks posed by commercial real estate, which have long been a concern of his, as a possible vector to amplify trouble.Without naming any firms, Mr. Rosengren noted the particular concerns posed by co-working companies. He made this comment as the parent of office-sharing firm WeWork postponed its initial public offering amid investor doubts about its valuation and concerns about its corporate governance.Office-sharing firms are particularly exposed to risks should the economy run into trouble, and could wound landlords in the process, Mr. Rosengren said.“In a downturn the co-working company would be exposed to the loss of tenant income, which puts both them and the property owner at risk if they cannot make lease payments to the owner of the building,” he said.“I am concerned that commercial real estate losses will be larger in the next downturn because of this growing feature of the real estate market, which could ultimately make runs and vacancies more likely due to this new leasing model,” Mr. Rosengren said.“The fact that the shared office model relies on small-company tenants with short-term leases, combined with the potential lack of recourse for the property owner, is potentially problematic in a recession. This also raises the issue of whether bank loans to property owners in cities with major penetration by co-working models could experience a higher incidence of default and greater loss-given-defaults than we have seen historically.”

Of course, he is right. As we concluded more explicitly, in a bankruptcy, all those obligations would be frozen and squeezed among all the other pre-petition claims, which of course means that the commercial real estate market of cities where WeWork is especially active – like New York and London (and Rosengren’s Boston) – would suddenly find itself paralyzed, as a deflationary tsunami is unleashed among one of the strongest performing markets since the financial crisis.

No comments:

Post a Comment