Since my pre-IPO post on WeWork, where I valued the company ahead of its then imminent offering, much has happened. The company’s IPO collapsed under the weight of its own pricing contradictions, and after a near-death experience, Softbank emerged as the savior, investing an additional $ 8 billion in the company, and taking a much larger stake in its equity. As the WeWork story continues to unfold, I am finding myself more interested in Softbank than in WeWork, largely because it’s actions cut to the heart of so many questions in investing, from how sunk costs can affect investing decisions, to the feedback effects from mark-to-market accounting, and finally on the larger question of whether smart money is really smart or just lucky.

WeWork: The IPO Aftermath

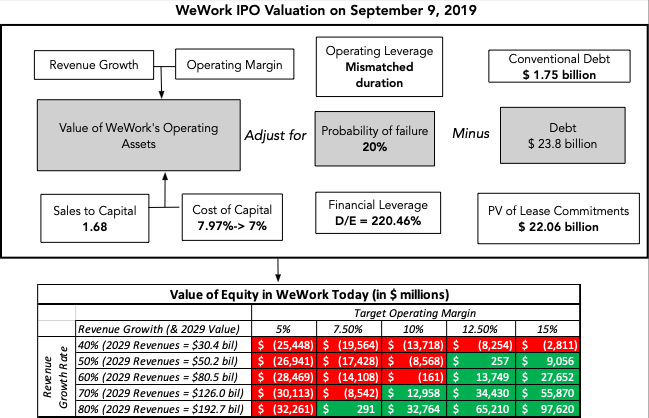

It has been only a few weeks since I valued WeWork for its IPO, but it seems much longer, simply because of how much has changed since then. As a reminder, I valued WeWork at about $10 billion pre-money, and $13.75 billion with the anticipated proceeds of $3.5 billion added on. I also argued that this was a company on a knife’s edge, a growth machine with immense operating and financial leverage, where misstep could very quickly tip them into bankruptcy, with a table illustrating how quickly the equity slips into negative territory, if the operating assumptions change:

|

| Download spreadsheet |

Soon after my post, the ground shifted under WeWork, as a combination of arrogance (on the part of VCs, bankers and founders) and business model risks caught up with the company, and the IPO was delayed, albeit reluctantly by the company. That action, though, left the company in a cash crunch, since it had been counting on the IPO to bring in $3 billion in capital to cover its near-term needs. In conjunction with a loss of trust in the top management of the company, created a vicious cycle with the very real possibility that the company would implode. As WeWork sought rescue packages, Softbank offered a lifeline, with three components to it:

- Equity Buyout: A tender offer of $3 billion in equity to buy out of existing stockholders in the firm to increase its share of the equity ownership to 80%. In an odd twist, Softbank contended that, after the financing, “it will not hold a majority of the voting rights… and does not control the company… WeWork will not be a subsidiary of Softbank. WeWork will be an associate of Softbank”. I am not sure whether this is a true confession of lack of control or a ploy to keep from consolidating WeWork (and its debt load) into Softbank’s financials.

- Added Capital: Softbank would provide fresh debt financing of $5 billion ($1.1 billion in secured notes, $2.2 billion in unsecured notes and $1.75 billion as a line of credit) and an acceleration of a $1.5 billion equity investment it had been planning to make into WeWork in 2020, giving WeWork respite, at least in the short term, from its cash constraints.

- Neutering Adam Neumann (at a cost): The offer also includes a severing of Adam Neumann’s leadership of the company, in return for which he will receive $1 billion in cash, $500 million as a loan to repay a JP Morgan credit line and $185 million for a four-year position as a consultant. I assume that the consulting fee is more akin to a restraining order, preventing him from coming within sighting distance of any WeWork office or building.

Since that deal was put together, the storyline has shifted, with Softbank now playing the lead role in this morality play, with multiple questions emerging:

- What motivated Softbank to invest so much more in a company where it had already lost billions? Some are arguing that Softbank had no choice, given the magnitude of what they had invested in WeWork, and others are countering that they were throwing good money after bad.

- With mark-to-market rules in effect at Softbank, how will accountants reflect the WeWork disaster on Softbank’s books? I think that fair-value accounting is neither fair nor is it about value, but the WeWork write down that Softbank had to take is a good time to discuss how fair-value accounting can have a feedback effect on corporate decision making.

- Is Masa Son a visionary genius or an egomaniac in need of checks and balances? A year ago, there were many who viewed Masa Son, with his 300-year plans and access to hundreds of billions of dollars in capital, was a man ahead of his time, epitomizing smart money. Today, the consensus view seems to be that he is an impulsive and emotional investor, not to be trusted in his investment judgments. The truth, as is often the case, lies somewhere in the middle.

- Since Softbank is a holding company, deriving a chunk of its value from its perceived ability to find start-ups and young companies and convert them into big wins, how will its value change as a result of its WeWork missteps? To answer this question, I will look at how Softbank’s market capitalization has changed over time, especially around the WeWork fiasco, and examine the consequences for its Vision fund plans.

Sunk Cost or Corporate Rescue!

In the years that WeWork was a private company, Softbank was, by far, the largest investor in the company. In August 2019, when the IPO was first announced, Softbank had not only been its largest capital provider, investing $7.5 billion in the company, but had also supplied the most recent round of capital, at a pricing of $47 billion. That lead-in, though, raises questions about the motives behind its decision to invest an extra $ 8 billion to keep WeWork afloat.

- It’s a corporate rescue: There are some who would argue that Softbank had no choice, since without an infusion of capital, WeWork was on a pathway to being worth nothing and that by investing its capital, Softbank would avoid that worst-case scenario. In fact, if you believe Softbank, with the infusion, WeWork has a pre-money value of $8 billion, with the infusion, and while that is a steep write down from the $47 billion pricing, it is still better than nothing.

- Good money chasing bad: The sunk cost principle, put simply, states that when you make an investment decision, your choice should be driven by its incremental effects and not by how much you have already expended leading up to that decision. In practice, though, investors seem to abandon this principle, trying to make up for past mistakes by making new ones. In the context of Softbank’s new WeWork investment, this would imply that Softbank is investing $ 8 billion in WeWork, not because it believes that it can generate more than that amount in incremental value from future cash flows, but because it had invested $7.5 billion in the past.

So, how do you resolve this question? As I see it, the Softbank rescue of WeWork may have helped it avoid a near term liquidity meltdown, but it has not addressed any of the underlying issues that I noted with the company’s business model. In fact, it has taken a highly levered company whose only pathway to survival was exponential growth and made it an even more levered company with constrained growth. In fact, Softbank has been remarkably vague about the economic rationale for the added investment and their story does not hold up to scrutiny. I do realize that Masa Son claims that “(t)he logic is simple. Time will resolve . . . and we will see a sharp V-shaped recovery,” in WeWork, but I don’t see the logic, time alone cannot resolve a $30 billion debt problem and there are enough costs in non-core businesses to cut to yield a quick recovery. At least from my perspective, Softbank’s investment in WeWork is good money chasing bad, a classic example of how sunk costs can skew decisions. To those who would counter that Softbank has a lot of money to lose and smart people working for it, note that the more money you have to lose and the smarter people think they are, the more difficult it becomes to admit to past mistakes, exacerbating the sunk cost problem. In fact, now that Softbank will have more than $15 billion invested in WeWork, they have made the sunk cost problem worse, going forward.

Accounting Fair Value

I understand the allure of fair value accounting to accountants. It provides them with a way to update the balance sheet, to reflect real world changes and developments, and make it more useful to investors. The fact that it also creates employment for accountants all over the world is a bonus, at least from their perspective. I think that the accounting response to Softbank’s WeWork mistake illustrates why fair value accounting is an oxymoron, more likely to do damage than good:

- It is price accounting, not value accounting: In Softbank’s latest earnings report, we saw the first installment of accounting pain from the WeWork mistake, with Softbank writing down its WeWork investment by $4.6 billion and reporting a hefty loss for the quarter. The reason for the write-down, though, was not a reassessment of WeWork’s value, but a reaction to the drop in the pricing of the company’s equity from the $47 billion before the IPO to $8 billion after the IPO implosion.

- With Softbank supplying the pricing: If you are dubious about the use of pricing in accounting revaluations, you should even more skeptical in this case, since Softbank was setting the pricing, at both the $47 billion pre-IPO, and the $8 billion, post-collapse. As I noted in the last section, there is nothing tangible that I can see in any of Softbank’s numerous press releases to back these numbers. In fact, if WeWork had not been exposed in its public offering, my guess is that Softbank would have probably invested more capital in the company, marked up the pricing to some number higher than $47 billion and that we would not be having this conversation.

- Too little, too late: As is always the case with accounting write-downs and impairments, there was very little news in the announcement. In fact, given that the write down was based upon pricing, not value, the market knew that a write off was coming and approximately how much the write off would be, which explains why even multi-billion write offs and impairments usually have no price effect, when announced. Incidentally, the accountants will offer you intrinsic valuations (DCF) to back up their assessments, but I would not attach to much weight to them, since they are what I call “kabuki valuations”, where the analysts decide, based on the pricing, what they would like to get as value, and then reverse engineer the inputs to deliver that number.

- With dangerous feedback effects: If all fair value accounting did was create these write downs and impairments that don’t faze investors, I could live with the consequences and treat the costs incurred in the process as a jobs plan for accountants. Unfortunately, companies still seem to think that these accounting charges are news that moves markets and take actions to minimize them. In fact, a cynic might argue that one motivation for Softbank’s rescue of WeWork was to minimize the write down from its mistake.

I am not a fan of fair value accounting, partly because it is a delayed reaction to a pricing change and is not a value reassessment, and partly because companies are often tempted to take costly actions to make their accounting numbers look better.

Smart Money, Stupid Money!

I hope that this entire episode will put to rest the notion of smart money, i.e., that there are investors who have access to more information than we do, have better analytical tools than the rest of us and use those advantages to make more money than the rest of us. In fact, it is this proposition that leads us to assume that anyone who makes a lot of money must be smart, and by that measure, Masa Son would have been classified as a smart investor, and wealthy investors funneled billions of dollars into Softbank Vision funds, on that basis. I am not going to argue that the WeWork misadventure makes Masa Son a stupid investor, but it does expose the fact that he is human, capable of letting his ego get ahead of good sense and that at least some of his success over time has to be attributed being in the right place at the right time.

So, if investors cannot be classified into smart and stupid, what is a better break down? One would be to group them into lucky and unlucky investors, but that implies a complete surrender to the forces of randomness that I am not yet willing to make. I think that investors are better grouped into humble and arrogant, with humble investors recognizing that success, when it comes, is as much a function of luck as it is of skill, and failure, when it too arrives, is part of investing and an occasion for learning. Arrogant investors claim every investing win as a sign of their skill and view every loss as an affront, doubling down on their mistakes. If I had to pick someone to manage my money, the quality that I would value the most in making that choice is humility, since humble investors are less likely to overpromise and overcommit. I think of the very act of demanding obscene fees for investment services is an act of arrogance, one reason that I find it difficult to understand why hedge funds are allowed to get away with taking 2% of your wealth and 20% of your upside.

Leading into the WeWork IPO, the question of where Masa Son fell on the humility continuum was easy to answer. Anyone who makes three hundred year plans and things that bigger is always better has a God complex, and success feeds that arrogance. I would like to believe that the WeWork setback has chastened Mr. Son, and in his remarks to shareholders this week, he said the right things, stating that he had “made a bad investment decision, and was deeply remorseful”, speaking of WeWork. However, he then undercut his message by not only claiming that the pathway to profit for WeWork would be simple (it is not) but also asserting that his Vision fund was still better than other venture capitalists in seeking out and finding promising companies. in my view, Masa Son needs a few more reminders about humility from the market, since neither his words nor his actions indicate that he has learned any lessons.

Softbank: The WeWork Effect

WeWork may have been Masa Son’s mistake, but the vehicle that he used to make the investment was Softbank, through the company and its Vision fund. As WeWork has unraveled, it is not surprising that Softbank has taken a significant hit in the market.

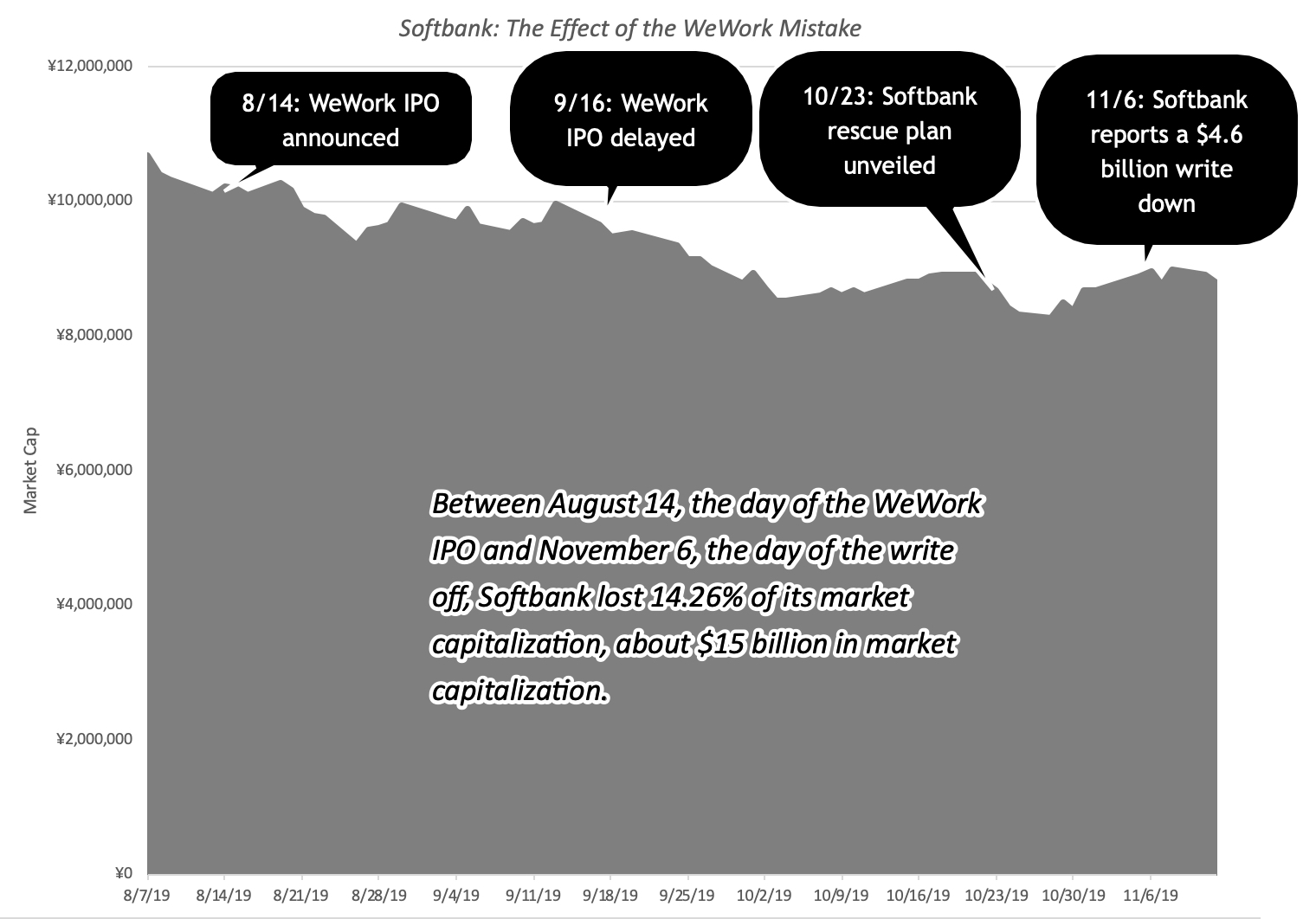

Note that Softbank has lost more than $15 billion in value since August 14, when the WeWork IPO was announced, and much of that loss can be attributed to the unraveling of the IPO, and how investor perceptions of Masa Son’s investing skills have changed since.

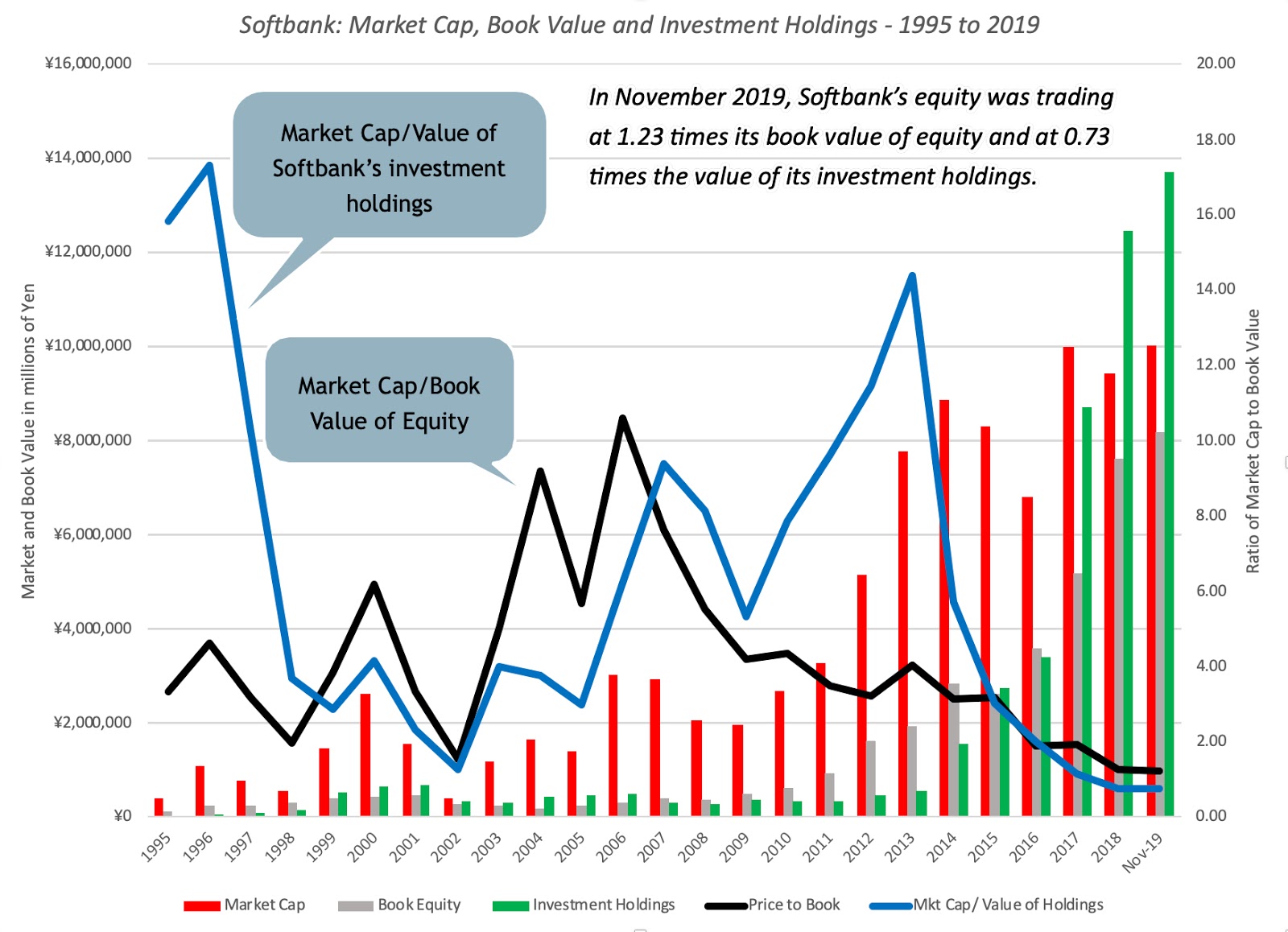

The knocking down of Softbank’s value by the market may strike some of you as excessive, but there is reason that Softbank’s WeWork investment has ripple effects. Softbank may be built around a telecom company, but like Berkshire Hathaway, the company that Masa Son is rumored to admire and aspire to be, it is a holding company for investments in other companies. In fact, its most valuable holding remains an early investment in Alibaba, now worth tens of billions dollars. While Alibaba is publicly traded and its pricing is observable, many of Softbank’s most recent investments have been in young, private companies like WeWork. With these investments, the pricing attached to them by Softbank, in its financials, comes from recent VC funding rounds and their valuations reflect trust in Softbank’s capacity to pick winners and the WeWork meltdown hurts on both counts. First, investors are more wary about trusting VC pricing, especially if Softbank has been a lead investor in funding rounds, since that is how you arrived at the $47 billion pricing for WeWork in the first place. Second, the notion of Masa Son as an investing savant, skilled at picking the winners of the disruption game, has been damaged, at least for the moment and perhaps irreparably. The easiest way to measure how investor perceptions have changed is to compare the market capitalization of Softbank to its book value, a significant proportion of which reflects its holdings, marked to market:

Investors have been wary of Softbank’s investing skills, even before the WeWork IPO, but the write offs on Uber and WeWork has made them even more skeptical, as the price to book ratio continues its march towards parity, with the market capitalization at 123% of the book value of equity in November 2019. In fact, if you focus just on Softbank’s non-consolidated holdings, public and private, note that the market capitalization of Softbank now stands at 73% of the value of just these holdings, most of which are marked to market. Put simply, when you buy Softbank, you are getting Uber and Alibaba at a discount on their traded market prices, but before you put your money down on what looks like a great deal, there are two considerations that may affect your decision. The first is that the company has a vast amount of debt on its balance sheet that has to be serviced, potentially putting your equity at risk, and the second is that you are getting Softbank (and Masa Son) as the custodian of the investments. If you have lost faith in Masa Son’s investing judgments (in people and in companies), you may view the 27% discount that the market is attaching to Softbank’s holdings as entirely justifiable and steer away from the stock. In contrast, if you feel that WeWork was an aberration in an otherwise stellar investment picking record, you should load up on Softbank stock. As for me, I don’t plan to own Softbank! I don’t like grandiosity and Masa Son seems to have been soaked in it.

YouTube Video

Blog Posts

No comments:

Post a Comment