Investors in agency mortgage-backed securities will find next year to be “anything but smooth sailing” as Fed rate hikes and balance sheet reduction will lead to an increase in real rates and volatility while pushing spreads wider, Bank of America Inc. MBS strategist team led by Satish Mansukhani write in a 2019 outlook report.

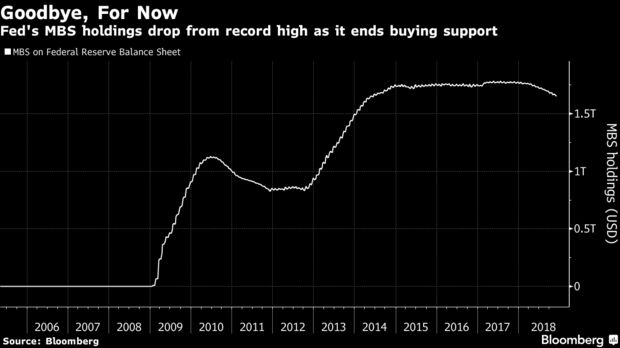

The key to 2019 sector performance will be the enthusiasm of relative value investors such as money managers to absorb the $375 billion demand gap created in part by the central bank’s exit. Compared to the pre-crisis era, money manager MBS holdings have declined $500 billion amid a $2.2 trillion growth in their assets under management. That suggests they are currently underweight mortgages.

This shift in sponsorship away from the central bank is likely to push spread volatility higher, though at its current level the MBS basis has already priced in a moderate increase. Combined with the retracement lower in real rates, Bank of America Inc. has shifted to a tactical overweight on mortgages. It sees an eventual widening of spreads and negative excess returns next year leading to a change to an underweight stance.

- From 2014 to 2018 ~85 percent of outstanding MBS were in the hands of the Fed, domestic banks, insurance companies and overseas buyers, explaining the highly subdued spread volatility

- Expect that to decline to 80 percent by end of next year on a combination of Fed runoff of $200 billion in 2019 from $150 billion this year, $228 billion in organic supply and forecast bank demand of $90 billion

- Three big “ifs” for next year are trade wars, bank regulatory proposals and money manager positioning in corporates versus MBS

- Escalation of trade war tensions may trigger a risk-off sentiment and increase the likelihood “for the Fed to exercise its put”

- Wild card for bank demand is regulatory outcomes. Most notably the Treasury’s proposal to ease eSLR ratios at the bank subsidiary levels

- Investor positioning and attractiveness versus credit all point to potential money manager demand

No comments:

Post a Comment